The adoption of environmental, social and governance (ESG) criteria is increasing, releasing capital for ESG compliant projects. Africa has vast potential for projects aligned with ESG related criteria which will achieve the United Nation’s sustainable development goals. There are many firms, innovations and projects, like The Green Economy Project, operating across Africa whose operations align with these criteria. Despite Africa’s rich natural resources, renewable energy potentials and human capital, connecting investors with investees regarding development opportunities is complicated. This results in missed opportunities and reduces the capacity of ESG investment to flow into projects in Africa that would otherwise support ESG investment mandates. The key to unlocking this potential is making investors comfortable with the risks typically associated with investing in developing markets and identifying sustainable investments that can deliver adequate returns.

Sustainable Investing in Africa:

Africa’s investment case is compelling. Sub-Saharan Africa’s GDP has been rising steadily, reaching $1.767 trillion in 2019 (Worldbank), driven by a quickly growing middle class. GDP in Africa did contract by 2.1% in 2020 due to COVID, however it is expected to completely recover and grow by 3.4% in 2021 (African Development Bank). Africa’s growth prospects lay upon improved macroeconomic policies, lower public debt, and greater political stability. However, as with the vast majority of Less Economically Developed Countries (LEDCs), there are significant barriers in the form of: poor infrastructure, weak regional infrastructure links, limited access to market information, failure of regulation, and small domestic markets.

Africa is developing a new look on sustainable investing. There is a growing awareness that sustainable investing can tackle the social and economic challenges in the region and that the resulting economic growth will be sustainable, benefitting investors in the long run. To this end, integrating ESG factors into investment is particularly important for developing countries, which have limited resources to adapt to urbanization and supply side shocks in the market.

African investor and business perspectives on ESG priorities are varied. Like other emerging markets, the private sector will play a positive role. A more compelling rationale towards sustainable investing would be for local investors to take the opportunity to grow new businesses where there are current vacancies.

Focusing on Private Equity:

Private equity is still small in Sub-Saharan Africa, but it is growing extremely quickly in response to improving economic fundamentals in the region. This trend is expected to continue with 92% of PE investors expecting an increase in PE investing into Sub-Saharan Africa over the next five years.

There are two common PE management models:

Development Finance Institutions (DFIs) have been one of the biggest contributors to funding PE mandates that integrate ESG into Africa. DFIs are financial institutions that provide risk capital for economic development projects on a non-commercial basis (Wikipedia). The DFI-PE relationship shows the fit between the PE asset class in Africa and the sustainable investment theme. The role and influence of DFIs in this space is growing. DFI capital is imperative for new funds being raised and remains important for subsequent funds however this diminishes once the investment team has a good track record. DFIs generally have long term horizons and a jurisdictional commitment. They can be notoriously slow through investment committees and contracting, but this means that they can manage the complexity and mitigate the risks of investing in an emerging market.

Removing Barriers to Sustainable Investment:

The barriers to sustainable investment in Africa are similar to many other regions:

A Battle for Power:

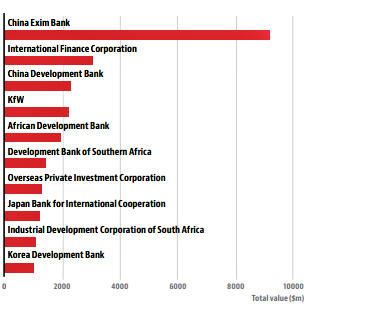

Africa’s huge potential, especially its rich natural resources and renewable energy prospects, has clearly been recognised by developed economies, with both the US and China increasing their DFI influence in the region. A clear example of this is the growing shift between bilateral and multilateral lending in the region. Bilateral lending has risen to prominence in Sub-Saharan Africa, occupying over 50% of the loans in a $35bn market (CICA), where more developed countries are looking to monopolise their influence. The use of bilateral loans cuts out the shared capital being loaned by multiple financial institutions, meaning multiple countries cannot work together to finance a certain project in the region. China started to implement this aggressively, loaning $19bn to energy and infrastructure projects in Africa between 2014-2017 (CICA), meaning China’s Exim Bank has

been the largest policy lender in the region between 2008-2017 (CICA).

Sustainable Investing in Africa:

Africa’s investment case is compelling. Sub-Saharan Africa’s GDP has been rising steadily, reaching $1.767 trillion in 2019 (Worldbank), driven by a quickly growing middle class. GDP in Africa did contract by 2.1% in 2020 due to COVID, however it is expected to completely recover and grow by 3.4% in 2021 (African Development Bank). Africa’s growth prospects lay upon improved macroeconomic policies, lower public debt, and greater political stability. However, as with the vast majority of Less Economically Developed Countries (LEDCs), there are significant barriers in the form of: poor infrastructure, weak regional infrastructure links, limited access to market information, failure of regulation, and small domestic markets.

Africa is developing a new look on sustainable investing. There is a growing awareness that sustainable investing can tackle the social and economic challenges in the region and that the resulting economic growth will be sustainable, benefitting investors in the long run. To this end, integrating ESG factors into investment is particularly important for developing countries, which have limited resources to adapt to urbanization and supply side shocks in the market.

African investor and business perspectives on ESG priorities are varied. Like other emerging markets, the private sector will play a positive role. A more compelling rationale towards sustainable investing would be for local investors to take the opportunity to grow new businesses where there are current vacancies.

Focusing on Private Equity:

Private equity is still small in Sub-Saharan Africa, but it is growing extremely quickly in response to improving economic fundamentals in the region. This trend is expected to continue with 92% of PE investors expecting an increase in PE investing into Sub-Saharan Africa over the next five years.

There are two common PE management models:

- Traditional financial investor with focus on financial engineering and selective changes in the governance model of portfolio companies

- Value creation through active ownership

Development Finance Institutions (DFIs) have been one of the biggest contributors to funding PE mandates that integrate ESG into Africa. DFIs are financial institutions that provide risk capital for economic development projects on a non-commercial basis (Wikipedia). The DFI-PE relationship shows the fit between the PE asset class in Africa and the sustainable investment theme. The role and influence of DFIs in this space is growing. DFI capital is imperative for new funds being raised and remains important for subsequent funds however this diminishes once the investment team has a good track record. DFIs generally have long term horizons and a jurisdictional commitment. They can be notoriously slow through investment committees and contracting, but this means that they can manage the complexity and mitigate the risks of investing in an emerging market.

Removing Barriers to Sustainable Investment:

The barriers to sustainable investment in Africa are similar to many other regions:

- Inertia in the status quo

- Poor regulation

- Inadequate data and disclosure

- Gaps in the investment chain

A Battle for Power:

Africa’s huge potential, especially its rich natural resources and renewable energy prospects, has clearly been recognised by developed economies, with both the US and China increasing their DFI influence in the region. A clear example of this is the growing shift between bilateral and multilateral lending in the region. Bilateral lending has risen to prominence in Sub-Saharan Africa, occupying over 50% of the loans in a $35bn market (CICA), where more developed countries are looking to monopolise their influence. The use of bilateral loans cuts out the shared capital being loaned by multiple financial institutions, meaning multiple countries cannot work together to finance a certain project in the region. China started to implement this aggressively, loaning $19bn to energy and infrastructure projects in Africa between 2014-2017 (CICA), meaning China’s Exim Bank has

been the largest policy lender in the region between 2008-2017 (CICA).

A graph showing the top policy lenders in Sub-Saharan Africa from 2008-2017. Source: Baker McKenzie

To respond to this, US decided to turn the Overseas Private Investment Corporation (OPIC) into the International Development Finance Corporation, simultaneously doubling its lending ceiling to $60bn (CICA).

Integrating ESG:

The heightened focus on Sub-Saharan Africa is certain to increase the flow of finance to the region, increasing infrastructure and benefitting its businesses and clients. However, a clear, systematic approach is important for ESG integration rather than a power struggle between the world’s strongest nations. The most important step is to make the case that sustainable investing can lead to increased returns and reduced risks across asset classes. Local knowledge is the best knowledge, so tapping into regional insights can lead to effective global best practices. Once ESG is integrated into Africa, monitoring performance against a sustainability index will be important, especially in volatile emerging markets. Unlocking this potential will not be easy, however if done effectively, it will open up long term growth in rapidly expanding economies for decades to come.

Zaiim Premji

Want to keep up with our most recent articles? Subscribe to our weekly newsletter here.

Integrating ESG:

The heightened focus on Sub-Saharan Africa is certain to increase the flow of finance to the region, increasing infrastructure and benefitting its businesses and clients. However, a clear, systematic approach is important for ESG integration rather than a power struggle between the world’s strongest nations. The most important step is to make the case that sustainable investing can lead to increased returns and reduced risks across asset classes. Local knowledge is the best knowledge, so tapping into regional insights can lead to effective global best practices. Once ESG is integrated into Africa, monitoring performance against a sustainability index will be important, especially in volatile emerging markets. Unlocking this potential will not be easy, however if done effectively, it will open up long term growth in rapidly expanding economies for decades to come.

Zaiim Premji

Want to keep up with our most recent articles? Subscribe to our weekly newsletter here.