Introduction

What is happening in China’s real estate sector? It used to be the country’s main driver of the economy, but it has started to drag it in the opposite direction. The property market has contracted by 7% year on year, causing many struggles to Chinese real estate companies, including Evergrande, the second largest one. The result is that developers are no longer building homes, buyers have started to hold off on paying their mortgages or entering the market, and the system has run out of capital. China’s plan consists in directing more state-owned money to solve the issue, but the question is: will this system still be sustainable in the long term?

China’s Property-driven Growth Model

Since the opening of its markets in 1980s, China’s property market has been a major driver of the economy. This is because, at that moment, China was seriously underinvested in property, infrastructure, and manufacturing capacity. Hence, the majority of the investments were productive as they contributed more to the economy than what they cost, fostering economic growth. Nowadays, the property market continues to be an important contributor to the economy, estimated at 17-29% of GDP, depending on the size of industry included. According to the People’s Bank of China (PBOC), direct investment in real estate in 2020 reached about RMB 7.5 trillion (US$1.18 trillion), contributing 7.4% to GDP. Moreover, as data provided by the National Bureau of Statistics (NBS) show, the construction industry contributed a further RMB 7.3 trillion (US$1.15 trillion), or 7.2 % of 2020’s GDP. In terms of investment, real estate lead 51.5% of investments in fixed assets nationwide, of which its development contributed 27.3% (Ren Zeping, chief economist at Soochow Securities, a financial services institute). Lastly, the construction sector in 2020 recorded more than 62 million jobs, thus demonstrating how enormous is the number of people whose livelihoods depends on it. Just by considering these data we can easily understand how a healthy property market is essential for Chinese economy.

The Three Red Lines

For most Chinese citizens the severity of the current situation in the housing market is evident, with tens if not hundreds of unfinished buildings located in most cities. Partially funded by individual families, these buildings would become home to those that had bought so-called ‘presale properties’, apartments sold at a lower price before they are physically constructed. However, the situation changed dramatically in the past two years and many of them are now left with no money and no home, as developers struggle to sustain funding for the construction of these buildings.

August 2020 marked the beginning of the downfall for many property developers, with the Chinese government implementing the ‘Three Red Lines’, a set of restrictions on the level of debt constructors could obtain. More specifically, companies needed to adhere to three rules: keep liabilities below 70% of assets, maintain a level of net debt not greater than equity, and have enough liquidity to pay off all short-term debt. The rules were imposed as the looming fear of a debt-driven property price bubble worried Chinese regulators. This, in turn, left many developers, who were using debt as a primary source of funding, with no means to finish their current projects.

As funds dwindled, construction on many pre-sold properties gradually ceased, leaving hundreds of thousands of future property owners without what they had paid for. Many chose to protest, boycotting their mortgage payments, adding fuel to a housing system that had already started burning down. In June 2022, the rating of most Chinese property developers had gone down, with more than 50% of them being below Caa1 rating or having no rating at all, compared to just 1% of developers one year ago. They have also failed to make payments on roughly $31bn of offshore bonds, and are facing a shortfall of business revenues as home sales have fallen by nearly 38% YoY in the week-long holiday beginning on October 1st.

August 2020 marked the beginning of the downfall for many property developers, with the Chinese government implementing the ‘Three Red Lines’, a set of restrictions on the level of debt constructors could obtain. More specifically, companies needed to adhere to three rules: keep liabilities below 70% of assets, maintain a level of net debt not greater than equity, and have enough liquidity to pay off all short-term debt. The rules were imposed as the looming fear of a debt-driven property price bubble worried Chinese regulators. This, in turn, left many developers, who were using debt as a primary source of funding, with no means to finish their current projects.

As funds dwindled, construction on many pre-sold properties gradually ceased, leaving hundreds of thousands of future property owners without what they had paid for. Many chose to protest, boycotting their mortgage payments, adding fuel to a housing system that had already started burning down. In June 2022, the rating of most Chinese property developers had gone down, with more than 50% of them being below Caa1 rating or having no rating at all, compared to just 1% of developers one year ago. They have also failed to make payments on roughly $31bn of offshore bonds, and are facing a shortfall of business revenues as home sales have fallen by nearly 38% YoY in the week-long holiday beginning on October 1st.

Local Governments’ Contagion

During this turmoil among property developers, the Chinese government and disappointed soon-to-be house owners, there was another element of the Chinese growth model that got the short end of the stick, local governments. Property developers generate a large chunk of the revenues local governments make by buying land needed for construction purposes. Thus, after developers’ funds were substantially reduced, there was little interest in these lands, and local governments soon began to struggle as well.

An important reason why this is extremely concerning for local governments is their extremely large level of debt. The main mechanism used to fund real estate development and local infrastructure projects in China is the so-called local government funding vehicle (LGFV), which generates capital through selling bonds with varying credit risk in the market. LGFV bonds made up a quarter of all corporate debt fundraising in China in 2021, according to Moody’s. LGFV issuance is substantially higher than a year ago, soaring 184% in April compared to last year, in an attempt to fill in the gap created by the restrictions the Three Red Lines imposed on corporate debt.

As a result, the system started being crunched on both sides as developers struggled to meet their current obligations and the pressure for local governments was mounting, as they faced cuts in revenues and much higher debt. In fact, most local governments will be facing funding gaps this year, meaning their revenues from all sources are likely to be lower than expenditures, which poses the risk of destabilizing the $7.8tn of LGFV debt present in China as of the end of 2021, creating potentially catastrophic consequences for the whole Chinese economy.

An important reason why this is extremely concerning for local governments is their extremely large level of debt. The main mechanism used to fund real estate development and local infrastructure projects in China is the so-called local government funding vehicle (LGFV), which generates capital through selling bonds with varying credit risk in the market. LGFV bonds made up a quarter of all corporate debt fundraising in China in 2021, according to Moody’s. LGFV issuance is substantially higher than a year ago, soaring 184% in April compared to last year, in an attempt to fill in the gap created by the restrictions the Three Red Lines imposed on corporate debt.

As a result, the system started being crunched on both sides as developers struggled to meet their current obligations and the pressure for local governments was mounting, as they faced cuts in revenues and much higher debt. In fact, most local governments will be facing funding gaps this year, meaning their revenues from all sources are likely to be lower than expenditures, which poses the risk of destabilizing the $7.8tn of LGFV debt present in China as of the end of 2021, creating potentially catastrophic consequences for the whole Chinese economy.

Evergrande, China’s Lehmann Moment

The crisis in the real estate market has had a major impact on one of China’s biggest property developers, Evergrande. In September 2021, investors started to consider the probability of a default for the developer due to a missed payment on an offshore bond, which was trading at $0.28 on the dollar, a signal of serious financial distress for Evergrande. The stock price had begun falling around April of the same year and did not show any signs of recovery, reaching record lows one month after the other. By December, one of Evergrande’s biggest peers, Kaisa Group, the world’s second most indebted property developer, also suspended trading on its stock, as it failed to make a payment on a $400mn bond.

For Evergrande, December marked the date it formally defaulted and the plan for its restructuring commenced. Evergrande’s restructuring was meant to dampen the effect of the collapse of one of China’s biggest firms in the real estate market. Few details were made public at the time, and the restructuring plan was characterized as a ‘Black Box’, but the primary goal was saving domestic homeowners investing in prepaid properties. Approximately six months later, Evergrande missed the deadline it had imposed to publish a preliminary restructuring proposal by the end of July. The restructuring plan still remains a mystery, but in the meantime, the situation for Evergrande does not look any brighter, as one of its creditors seized their headquarters after Evergrande defaulted on its debt.

Speculators are starting to draw parallels between Evergrande’s precarious position and the downfall of Lehman Brothers marking the climax of the 2007-2008 financial crisis. Similar to what happened 15 years ago, the causes of the crisis slowly accumulated several years prior to the fall of one of the big names, and Evergrande’s default is only a wake-up call for those that had not already realized the severity of the situation. The future of Evergrande is anything but clear, as all investors eyeball one of the biggest and most important restructurings of all time. Whether China will be able to salvage the situation or whether Evergrande’s bankruptcy will mark the beginning of a large scale economic crisis, is the question in everyone’s mind at the moment, but as we have witnessed, the answer is nearly impossible to find.

For Evergrande, December marked the date it formally defaulted and the plan for its restructuring commenced. Evergrande’s restructuring was meant to dampen the effect of the collapse of one of China’s biggest firms in the real estate market. Few details were made public at the time, and the restructuring plan was characterized as a ‘Black Box’, but the primary goal was saving domestic homeowners investing in prepaid properties. Approximately six months later, Evergrande missed the deadline it had imposed to publish a preliminary restructuring proposal by the end of July. The restructuring plan still remains a mystery, but in the meantime, the situation for Evergrande does not look any brighter, as one of its creditors seized their headquarters after Evergrande defaulted on its debt.

Speculators are starting to draw parallels between Evergrande’s precarious position and the downfall of Lehman Brothers marking the climax of the 2007-2008 financial crisis. Similar to what happened 15 years ago, the causes of the crisis slowly accumulated several years prior to the fall of one of the big names, and Evergrande’s default is only a wake-up call for those that had not already realized the severity of the situation. The future of Evergrande is anything but clear, as all investors eyeball one of the biggest and most important restructurings of all time. Whether China will be able to salvage the situation or whether Evergrande’s bankruptcy will mark the beginning of a large scale economic crisis, is the question in everyone’s mind at the moment, but as we have witnessed, the answer is nearly impossible to find.

The Numbers of the Bubble

What’s the situation now, a little more than a year after Evergrande’s collapse?

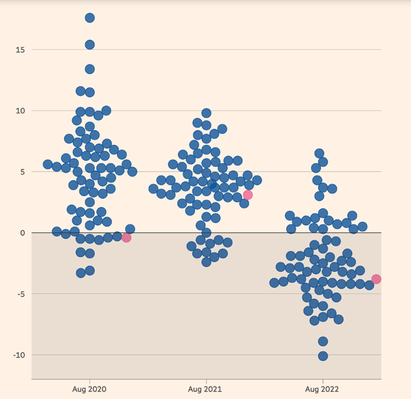

Prices for new homes in 70 Chinese cities fell by 1.3% year on year in August, worse than expected and still in line with the turbulent last 12 months in which the sector, from being the main driver of growth, became the major threat to the fastest-growing country in the world. Furthermore, a third of the total of property loans are now classed as bad debt, -29.1%, coming from a 24.3% at the end of last year, according to research conducted by Citigroup. The crisis is so gigantic that the government’s decision to put 200bn yuan (£26bn) to kickstart investment was judged by analysts to be way less of what was actually needed. As a matter of fact, S&P said that at least 800bn yuan would be needed. Moreover, nearly 2m homes are unfinished across all Chinese territory and homebuyers are refusing to pay their mortgages across uncompleted projects until developers finish construction on the apartments. “China’s property sales are set to plunge this year by more than they did during the 2008 financial crisis” said S&P Global Ratings. The crisis’s numbers are enormous and also other countries are starting to be worried.

Prices for new homes in 70 Chinese cities fell by 1.3% year on year in August, worse than expected and still in line with the turbulent last 12 months in which the sector, from being the main driver of growth, became the major threat to the fastest-growing country in the world. Furthermore, a third of the total of property loans are now classed as bad debt, -29.1%, coming from a 24.3% at the end of last year, according to research conducted by Citigroup. The crisis is so gigantic that the government’s decision to put 200bn yuan (£26bn) to kickstart investment was judged by analysts to be way less of what was actually needed. As a matter of fact, S&P said that at least 800bn yuan would be needed. Moreover, nearly 2m homes are unfinished across all Chinese territory and homebuyers are refusing to pay their mortgages across uncompleted projects until developers finish construction on the apartments. “China’s property sales are set to plunge this year by more than they did during the 2008 financial crisis” said S&P Global Ratings. The crisis’s numbers are enormous and also other countries are starting to be worried.

House prices in August fall in nearly three-quarters of large Chinese cities

New home price in 70 cities, year-on-year change (%)

Financial Times

New home price in 70 cities, year-on-year change (%)

Financial Times

The Future of the Chinese Real Estate Market

Forecasts and predictions point to a grim future for the Chinese Real Estate market.

Recent reports show that more than 30 real estate firms defaulted on internationally sourced debt as of late August 2022, with several developers stating an anticipated 90% decrease in profit. Country Garden Holdings Co., one of the top developers in the Chinese real estate market judging by contracted sales, reported a 96% decrease in first-half profit, struggling to overcome the evident and widespread crisis of confidence that had thus far wreaked havoc on buyer and investor activity within the market. The severity of the situation is also perfectly reflected in the significant drop in profitability of the largest bad-debt management firms, such as China Cinda Asset Management Co. and China Huarong Asset Management Co. The lack of buyer and investor confidence has created a negative feedback loop within the market, especially considering the mortgage boycott, pushing developers to make the choice between using their “dwindling cash flow” to finish ongoing construction projects or to pay off their debts, the Financial Times reports. It is also important to mention the policy of the Chinese Communist Party and Xi Jinping’s anti-speculationist stance, which increases the likelihood of moderation when it comes to the price front. This conjecture of aforementioned factors is expected to lead to a 1.4% fall in home prices this year, according to a survey conducted by Reuters. Highly probable consequences include a “negative wealth effect”, a potential threat to the larger stability of the society and economy. It also goes without saying that confidence in the pre-sale model has been altogether done away with. All the meanwhile, voices such as that of the chairman of Country Garden Holdings Co., expect the market to “return to a stage of healthy development” by June 2023, reiterating the resilience of China’s economy and its ongoing process of urbanization that guarantee the long-term survival of the real estate industry in the country, according to the Wall Street Journal. On a structural level, the transformations the Real Estate industry is undergoing are ultimately resulting in the contraction of the market share of private developers, favoring instead the presence of state-owned developers. Overall, the supply and price-related factors previously discussed have resulted in the reduction of the importance of the property sector to the Asia-US dollar credit asset class as well as an accentuated decrease in overall debt issuance. Analysis done by Fund Selector Asia predicts a stabilization of the situation over time, noting, however, that surviving developers will see “more modest profit margins [and] more stable operations”, resulting in “healthier” balance sheets.

Recent reports show that more than 30 real estate firms defaulted on internationally sourced debt as of late August 2022, with several developers stating an anticipated 90% decrease in profit. Country Garden Holdings Co., one of the top developers in the Chinese real estate market judging by contracted sales, reported a 96% decrease in first-half profit, struggling to overcome the evident and widespread crisis of confidence that had thus far wreaked havoc on buyer and investor activity within the market. The severity of the situation is also perfectly reflected in the significant drop in profitability of the largest bad-debt management firms, such as China Cinda Asset Management Co. and China Huarong Asset Management Co. The lack of buyer and investor confidence has created a negative feedback loop within the market, especially considering the mortgage boycott, pushing developers to make the choice between using their “dwindling cash flow” to finish ongoing construction projects or to pay off their debts, the Financial Times reports. It is also important to mention the policy of the Chinese Communist Party and Xi Jinping’s anti-speculationist stance, which increases the likelihood of moderation when it comes to the price front. This conjecture of aforementioned factors is expected to lead to a 1.4% fall in home prices this year, according to a survey conducted by Reuters. Highly probable consequences include a “negative wealth effect”, a potential threat to the larger stability of the society and economy. It also goes without saying that confidence in the pre-sale model has been altogether done away with. All the meanwhile, voices such as that of the chairman of Country Garden Holdings Co., expect the market to “return to a stage of healthy development” by June 2023, reiterating the resilience of China’s economy and its ongoing process of urbanization that guarantee the long-term survival of the real estate industry in the country, according to the Wall Street Journal. On a structural level, the transformations the Real Estate industry is undergoing are ultimately resulting in the contraction of the market share of private developers, favoring instead the presence of state-owned developers. Overall, the supply and price-related factors previously discussed have resulted in the reduction of the importance of the property sector to the Asia-US dollar credit asset class as well as an accentuated decrease in overall debt issuance. Analysis done by Fund Selector Asia predicts a stabilization of the situation over time, noting, however, that surviving developers will see “more modest profit margins [and] more stable operations”, resulting in “healthier” balance sheets.

Broader Effects on the Chinese Economy

In an interview offered to the Financial Times, Partner at Rhodium Group, Logan Wright, partner at Rhodium Group suggested that “[the] next stage of the property crisis is the transmission of losses from property developers to China’s financial system”.

China’s strict COVID policy and the crisis in the property market are referenced as the two main factors causing the slowdown of its economic growth, which is set to take place at the slowest rate since 1990, save for 2020. World Bank forecasts suggest that the country’s economic output this year is set to lag behind other countries in Asia, with GDP growth decreasing from 8.1% last year to 2.8% this year, in comparison to the rest of the APAC area, set to grow at 5.3%. Real Estate accounts for around 29% of China’s GDP, and it is where 15% of workers are employed, suggesting the ample socio-economic implications of its volatility.

The debt crisis combined with the structural fragility present in the economy are devastating to the confidence of multinationals and investors operating in China in the country’s stock markets, a truth referenced in the paper recently issued by the European Chamber of Commerce in China, according to which “China was quickly losing ‘its allure as an investment destination’”, as reported by the Financial Times.

The crisis has also prompted developers to halt land purchases, decreasing, in turn, local governments’ revenue from tax and limiting their ability to invest in further development and infrastructure projects, and to pay back existing institutional debt as well. It is also worthwhile to mention the severity of the debt crisis in particular. The mountain of debts composed by LGFVs is currently valued at $7.8 trillion, or half of China’s GDP in 2021. Therefore, as defaults become an increasingly concrete and likely prospect, analysts predict the increasingly probable destabilization of LGFV debt as a whole. This, in turn, would prompt a “flight to safety” and may lead to the reinforcement of regional disparities as the total funding gap widens, threatening Yunnan, Fujian, Sichuan, and Guangxi especially. The threat of defaults only promises to destabilize this, with catastrophic implications on a macroeconomic level. Recently, the Chinese government has been facilitating access to bonds from healthier developers, which has helped keep stock prices somewhat afloat. There is consensus among analysts studying the ongoing phenomenon that, without a more comprehensive course of action pursued by the government, the situation will only continue to decline, dragging the integrity of the Chinese economy along with it.

China’s strict COVID policy and the crisis in the property market are referenced as the two main factors causing the slowdown of its economic growth, which is set to take place at the slowest rate since 1990, save for 2020. World Bank forecasts suggest that the country’s economic output this year is set to lag behind other countries in Asia, with GDP growth decreasing from 8.1% last year to 2.8% this year, in comparison to the rest of the APAC area, set to grow at 5.3%. Real Estate accounts for around 29% of China’s GDP, and it is where 15% of workers are employed, suggesting the ample socio-economic implications of its volatility.

The debt crisis combined with the structural fragility present in the economy are devastating to the confidence of multinationals and investors operating in China in the country’s stock markets, a truth referenced in the paper recently issued by the European Chamber of Commerce in China, according to which “China was quickly losing ‘its allure as an investment destination’”, as reported by the Financial Times.

The crisis has also prompted developers to halt land purchases, decreasing, in turn, local governments’ revenue from tax and limiting their ability to invest in further development and infrastructure projects, and to pay back existing institutional debt as well. It is also worthwhile to mention the severity of the debt crisis in particular. The mountain of debts composed by LGFVs is currently valued at $7.8 trillion, or half of China’s GDP in 2021. Therefore, as defaults become an increasingly concrete and likely prospect, analysts predict the increasingly probable destabilization of LGFV debt as a whole. This, in turn, would prompt a “flight to safety” and may lead to the reinforcement of regional disparities as the total funding gap widens, threatening Yunnan, Fujian, Sichuan, and Guangxi especially. The threat of defaults only promises to destabilize this, with catastrophic implications on a macroeconomic level. Recently, the Chinese government has been facilitating access to bonds from healthier developers, which has helped keep stock prices somewhat afloat. There is consensus among analysts studying the ongoing phenomenon that, without a more comprehensive course of action pursued by the government, the situation will only continue to decline, dragging the integrity of the Chinese economy along with it.

Conclusion

Given the importance of China’s contribution to the global economy, accounting for 28% of worldwide GDP growth between 2013 and 2018, its economic slowdown carries important consequences, and is set to increase the vulnerability of the world’s economy. Within the larger APAC area, recovery seems to be incoming, as there is high investor interest in real estate in places such as Australia, Singapore, and Japan. The crisis currently plaguing China’s Real Estate market has exposed severe systemic shortcomings that are of a profoundly structural nature. The responses adopted by the Chinese government appear feeble, and, consequently, the future of the market is still unclear. What is, however, clear, is that this marks a turning point in China’s long-time reign as an economic growth powerhouse. Extremely consequential on a global macroeconomic level, the future evolution of this situation ought to be monitored with great interest and concern.

Written by Livia Figarolo di Gropello, Georgia-Alesia Mirica, Delvi Hamzaraj.

Bibliography

https://www.aljazeera.com/economy/2022/11/1/chinas-property-slump-continues-in-october-as-prices-fall

https://www.ft.com/content/e9e8c879-5536-4fbc-8ec2-f2a274b823b4

https://www.ft.com/content/68286d3b-cd80-45f6-937d-7bd4dd7bd273

https://www.ft.com/content/dc75dd68-195d-48fe-b63c-da192ce5b81c

https://www.ft.com/content/9739c1cf-e7fd-4a32-95a1-3289de6b0367

https://www.bloomberg.com/news/articles/2022-10-31/china-home-sales-drop-28-as-covid-flare-up-adds-to-risks

https://capital.com/china-property-price-crash-investment-economic-slowdown

https://www.economist.com/leaders/2022/09/15/chinas-property-crisis-hasnt-gone-away-it-is-getting-worse

https://www.cnbc.com/2022/10/25/china-property-why-beijing-wont-bail-out-its-real-estate-sector.html

https://www.theguardian.com/business/2022/sep/25/china-property-bubble-evergrande-group

https://www.theguardian.com/business/2022/sep/25/china-property-bubble-evergrande-group

https://www.ft.com/content/e9e8c879-5536-4fbc-8ec2-f2a274b823b4

https://www.wsj.com/articles/chinas-housing-market-is-still-on-life-support-11663329147

https://fundselectorasia.com/what-does-the-future-hold-for-china-property/

https://www.wsj.com/articles/in-chinas-property-sector-there-is-nowhere-to-hide-11666179702

https://www.wsj.com/articles/china-abruptly-delays-gdp-release-during-communist-party-conference-11666000383?mod=article_inline

https://www.wsj.com/articles/chinas-property-market-has-slid-into-severe-depression-real-estate-giant-says-11661863259?mod=article_inline

https://asia.nikkei.com/Business/Markets/China-debt-crunch/Ripple-effect-of-China-real-estate-crisis-risks-bigger-economic-blow

https://www.nuveen.com/global/insights/real-estate/asia-pacific-is-well-placed-to-ride-out-the-storm

https://www.ft.com/content/e9e8c879-5536-4fbc-8ec2-f2a274b823b4

https://www.ft.com/content/68286d3b-cd80-45f6-937d-7bd4dd7bd273

https://www.ft.com/content/dc75dd68-195d-48fe-b63c-da192ce5b81c

https://www.ft.com/content/9739c1cf-e7fd-4a32-95a1-3289de6b0367

https://www.bloomberg.com/news/articles/2022-10-31/china-home-sales-drop-28-as-covid-flare-up-adds-to-risks

https://capital.com/china-property-price-crash-investment-economic-slowdown

https://www.economist.com/leaders/2022/09/15/chinas-property-crisis-hasnt-gone-away-it-is-getting-worse

https://www.cnbc.com/2022/10/25/china-property-why-beijing-wont-bail-out-its-real-estate-sector.html

https://www.theguardian.com/business/2022/sep/25/china-property-bubble-evergrande-group

https://www.theguardian.com/business/2022/sep/25/china-property-bubble-evergrande-group

https://www.ft.com/content/e9e8c879-5536-4fbc-8ec2-f2a274b823b4

https://www.wsj.com/articles/chinas-housing-market-is-still-on-life-support-11663329147

https://fundselectorasia.com/what-does-the-future-hold-for-china-property/

https://www.wsj.com/articles/in-chinas-property-sector-there-is-nowhere-to-hide-11666179702

https://www.wsj.com/articles/china-abruptly-delays-gdp-release-during-communist-party-conference-11666000383?mod=article_inline

https://www.wsj.com/articles/chinas-property-market-has-slid-into-severe-depression-real-estate-giant-says-11661863259?mod=article_inline

https://asia.nikkei.com/Business/Markets/China-debt-crunch/Ripple-effect-of-China-real-estate-crisis-risks-bigger-economic-blow

https://www.nuveen.com/global/insights/real-estate/asia-pacific-is-well-placed-to-ride-out-the-storm