Introduction

On 30th August 2020, Veolia, the French waste management, water and energy company made a bid to acquire 29.9% of Suez held by the utility shareholder Engie for €2.9bn. On 30th September 2020, Veolia raised the bid for the stake to €3.3bn, which was later accepted by Engie on 5th October 2020. Veolia’s initial offer was meant as the first step followed by the launch of a full bid to Suez, which was announced on 7th January 2021. To counter the potential takeover Suez cooperated with Ardian and GIP to launch a counter-offer. The merge of the two French groups would lead to the creation of the world champion of ecological transformation benefitting from the complementarities in technology and capabilities that would allow to succeed in the green transformation. After a series of legal battles and destructive strategies to prevent the completion of the bid, the deal has moved towards a hostile takeover, first in France in the last five years, which was rejected by the BoD of Suez at the end of February. Rejection of hostile takeover significantly complicates the situation taking into consideration significant ownership of Veolia in Suez (29.9%) and Veolia’s solid determination to acquire control. The complicated situation even started to attract attention of the French government officials, with the finance minister pushing for peaceful negotiations.

Industries Overview

Waste Management Industry

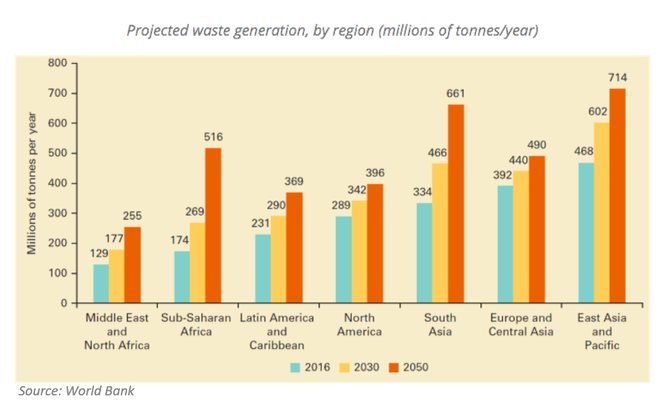

The waste management industry has experienced rapidly increasing demand in recent years due to ever-growing industrialization, global populations and demand for consumer goods. According to the World Bank, urban populations produce approximately 2.01bn tonnes of municipal solid waste annually, a number that is expected to grow 70%, to 3.4bn tonnes, by 2050. Similarly, industrial waste and hazardous waste production has also been increasing, most notably in low-income and middle-income countries, where more than half of waste is openly dumped. Thus, there has been a growingly urgent need for the management of solid wastes on a global scale.

On 30th August 2020, Veolia, the French waste management, water and energy company made a bid to acquire 29.9% of Suez held by the utility shareholder Engie for €2.9bn. On 30th September 2020, Veolia raised the bid for the stake to €3.3bn, which was later accepted by Engie on 5th October 2020. Veolia’s initial offer was meant as the first step followed by the launch of a full bid to Suez, which was announced on 7th January 2021. To counter the potential takeover Suez cooperated with Ardian and GIP to launch a counter-offer. The merge of the two French groups would lead to the creation of the world champion of ecological transformation benefitting from the complementarities in technology and capabilities that would allow to succeed in the green transformation. After a series of legal battles and destructive strategies to prevent the completion of the bid, the deal has moved towards a hostile takeover, first in France in the last five years, which was rejected by the BoD of Suez at the end of February. Rejection of hostile takeover significantly complicates the situation taking into consideration significant ownership of Veolia in Suez (29.9%) and Veolia’s solid determination to acquire control. The complicated situation even started to attract attention of the French government officials, with the finance minister pushing for peaceful negotiations.

Industries Overview

Waste Management Industry

The waste management industry has experienced rapidly increasing demand in recent years due to ever-growing industrialization, global populations and demand for consumer goods. According to the World Bank, urban populations produce approximately 2.01bn tonnes of municipal solid waste annually, a number that is expected to grow 70%, to 3.4bn tonnes, by 2050. Similarly, industrial waste and hazardous waste production has also been increasing, most notably in low-income and middle-income countries, where more than half of waste is openly dumped. Thus, there has been a growingly urgent need for the management of solid wastes on a global scale.

Furthermore, the business outlook of the waste treatment industry is being propelled due to the introduction and implementation of stringent environmental mandates. Currently, most developed countries are trying to raise investments across the recycling and composting industry, in compliance with the aforementioned regulations. This has driven significant efforts toward the improvement of traditional waste management services to advanced disposal and treatment services that have augmented the market size.

However, there exist high costs in producing and operating waste management solutions, especially for low-income and middle-income countries where waste management takes up 20% of local budgets. This is expected to hinder the market growth. Consequently, several waste management companies, including Suez and Veolia, have adopted strategies such as acquisitions and partnerships to offer better services in the market and to gain a competitive edge by driving optimal efficiency and maximizing market share.

However, there exist high costs in producing and operating waste management solutions, especially for low-income and middle-income countries where waste management takes up 20% of local budgets. This is expected to hinder the market growth. Consequently, several waste management companies, including Suez and Veolia, have adopted strategies such as acquisitions and partnerships to offer better services in the market and to gain a competitive edge by driving optimal efficiency and maximizing market share.

Finally, COVID-19 restrictions have created new considerations for the waste management industry. Waste production drastically declined from other industries and commercial sectors as many businesses were shut-down. Conversely, municipal waste increased from residential areas. However, industrial waste dominates the market in terms of revenues, causing the fall in demand for waste management to be sorely felt by the industry. Thankfully, the emergence of vaccines for coronavirus and the reopening of production facilities have kick-started the re-initiation of full-scale capabilities of waste management companies.

Water Management Industry

The water management industry’s size is ever-expanding across all of its sectors, owing to the declining availability of freshwater, primarily in the Middle East, Africa and Asia Pacific. This is anticipated to propel the need to treat wastewater globally.

The demand for water has been growing consistently due to rapid urbanization, rising population levels, economic development and industrial activities. Coupled with changing climate patterns and energy generation, the water treatment industry and all of its sectors (chemicals, technologies etc.) are highly sought after in the context of the world’s struggle to provide accessible freshwater to all populations. Water use has been increasing worldwide by about 1% annually since the 1980s and will most likely continue at a similar rate until 2050. Currently, 2bn people live in countries with high water stress and 4bn people will experience severe water scarcity one moth of the year. Thus, freshwater availability depends on wastewater treatment.

Veolia and Suez are significant players in the water management industry. Indeed, Suez currently owns the world’s largest research and development programme for water technology and is considered a pioneer in water resource management, conserving billions of gallons of water annually. Similarly, Veolia is a water treatment giant, with a portfolio of more than 350 technologies, ranging from online diagnostic solutions to evaporation and crystallization, energy-producing sludge treatments and state-of-the-art desalinization services as well as many more.

The water management industry’s size is ever-expanding across all of its sectors, owing to the declining availability of freshwater, primarily in the Middle East, Africa and Asia Pacific. This is anticipated to propel the need to treat wastewater globally.

The demand for water has been growing consistently due to rapid urbanization, rising population levels, economic development and industrial activities. Coupled with changing climate patterns and energy generation, the water treatment industry and all of its sectors (chemicals, technologies etc.) are highly sought after in the context of the world’s struggle to provide accessible freshwater to all populations. Water use has been increasing worldwide by about 1% annually since the 1980s and will most likely continue at a similar rate until 2050. Currently, 2bn people live in countries with high water stress and 4bn people will experience severe water scarcity one moth of the year. Thus, freshwater availability depends on wastewater treatment.

Veolia and Suez are significant players in the water management industry. Indeed, Suez currently owns the world’s largest research and development programme for water technology and is considered a pioneer in water resource management, conserving billions of gallons of water annually. Similarly, Veolia is a water treatment giant, with a portfolio of more than 350 technologies, ranging from online diagnostic solutions to evaporation and crystallization, energy-producing sludge treatments and state-of-the-art desalinization services as well as many more.

Consequently, the implementation of stringent environmental regulations has created new trends within the industry. Companies are moving away from groundwater pumping and towards more sustainable alternatives, as water reuse is becoming a more widespread practice along with desalination.

However, high costs are associated with the operation of treatment processes, including maintenance, energy and pollution, which have been a hindrance to market growth. Many treatment solutions are not available in low-income and middle-income countries, where water treatment is most needed. Nonetheless, the Asia-Pacific water treatment market is projected to grow with rapid industrialization driving the market landscape. Similarly, the European market, as well as the distillation, filtration and residential water management markets, have notable growth forecasts on account of technological advancements, rising health awareness and higher efficiency.

Energy Industry

The global energy as a service market size was worth $58.04bn in 2019 with a CAGR of 14.6% over the 2020-2027 forecast period.

In the last several years, the industry has experienced a decline in the growth rate of global energy demand, attributed to slower economic growth as well as milder weather conditions. This was disproportionately felt by coal and gas, while renewables and natural gas gained market share, with gas reaching 23% and renewables 14%, demonstrating gradual energy transition in practice.

However, high costs are associated with the operation of treatment processes, including maintenance, energy and pollution, which have been a hindrance to market growth. Many treatment solutions are not available in low-income and middle-income countries, where water treatment is most needed. Nonetheless, the Asia-Pacific water treatment market is projected to grow with rapid industrialization driving the market landscape. Similarly, the European market, as well as the distillation, filtration and residential water management markets, have notable growth forecasts on account of technological advancements, rising health awareness and higher efficiency.

Energy Industry

The global energy as a service market size was worth $58.04bn in 2019 with a CAGR of 14.6% over the 2020-2027 forecast period.

In the last several years, the industry has experienced a decline in the growth rate of global energy demand, attributed to slower economic growth as well as milder weather conditions. This was disproportionately felt by coal and gas, while renewables and natural gas gained market share, with gas reaching 23% and renewables 14%, demonstrating gradual energy transition in practice.

Indeed, despite the global pandemic as well as the onset of an economic recession, many countries as well as businesses have announced the implementation of decarbonization plans. For example, companies like Suez have been actively participating in the transition to renewable energy by providing means for water quality treatment, supplying operation and maintenance services and decommissioning maintenance services, which allow governments and companies to abide by stringent environmental mandates.

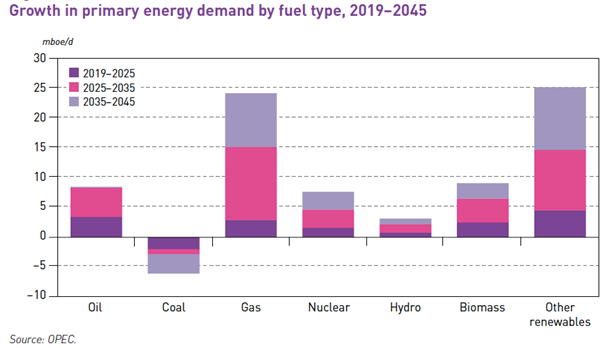

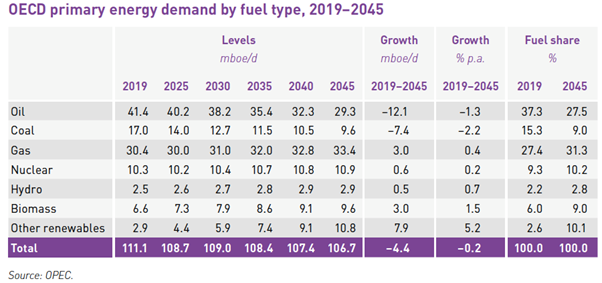

It is notable that OECD countries are the driving force of the transition to renewable energy. Indeed, in the next 30 years, hydropower and other renewables will experience decisive growth (0.7% p.a. and 5.2% p.a.), as OECD countries deploy more efficient and low-emission energy technology solutions.

It is notable that OECD countries are the driving force of the transition to renewable energy. Indeed, in the next 30 years, hydropower and other renewables will experience decisive growth (0.7% p.a. and 5.2% p.a.), as OECD countries deploy more efficient and low-emission energy technology solutions.

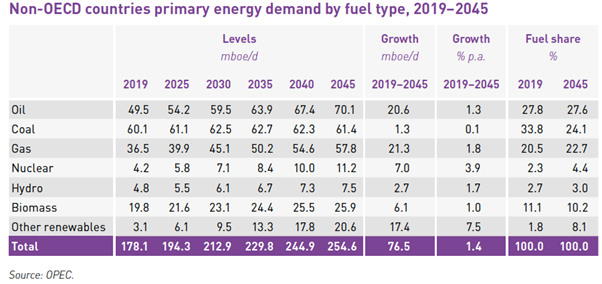

Conversely, the non-OECD energy mix is dominated by fossil fuels whose demand is projected to grow at a steady average of 1.4% p.a. over the forecast period (2019-2045). Nonetheless, the gradual expansion of renewables and nuclear energy suggests a possible acceleration in the transition to renewable energy further in the future

However, the energy industry was dealt a serious blow by the COVID-19 restrictions. Globally, energy demand declined by 3.8% in the first quarter of 2020. Coal demand fell by almost 8% compared with 2019, while natural gas demand declined by 2%. Renewables were the only energy sources that experienced a growth in demand, driven by priority dispatch and larger installed capacity. Consequently, global energy demand is expected to be suppressed until 2023, when it projected to return to its pre-COVID-19 levels.

The impact was felt within the industry through value chains, as most energy companies lost substantial revenues. The effect of declining demand also invoked lower energy prices, dealing the industry a second hit. However, the COVID-19 crisis is influencing the path for the conversion to clean energy, paving the way for a champion of global ecological transformation.

Main Involved Parties

Suez

Suez is the largest provider of equipment and services for drinkable water supply worldwide. Based in La Défense, Paris, the company operates in the utilities industry, with a strong focus on three segments, namely Water, Recycling and Recovery, Environmental Technologies and Solutions. This strategy is supported by a lean corporate structure, which defines resource allocation and organizes technical expertise. The company was originally an operating division of Suez, and it was only after the 2008 merger, which created GDF Suez (currently Engie S.A.), that it was separated as a stand-alone entity. After the IPO of the same year, Suez Environment’ shares skyrocketed reaching 40% in value on the very first day. In July 2015, after the group GDF Suez changed its name to Engie, the brand Suez Environment was simplified to simply Suez. Moreover, in September of the same year, it acquired a 40% stake in Sembcorp to provide water and waste management in Australia and in October 2017 it bought the Water & Process Technologies unit from GE Power, thus forming the new Water Technologies & Solutions business unit.

Until recent events, Engie, a French multinational company and global provider of electricity, gas and associated energy and environment services throughout the world, has been the largest shareholder of Suez, with an almost 35% stake (which in 2020 was sold to Veolia). Other major shareholders include Criteria Caixa (6%), Inversiones Los Canelos (3.6%) and Caltagirone Group (3.5%). Moreover, 51.8% of the total shares of the company are free float.

The impact was felt within the industry through value chains, as most energy companies lost substantial revenues. The effect of declining demand also invoked lower energy prices, dealing the industry a second hit. However, the COVID-19 crisis is influencing the path for the conversion to clean energy, paving the way for a champion of global ecological transformation.

Main Involved Parties

Suez

Suez is the largest provider of equipment and services for drinkable water supply worldwide. Based in La Défense, Paris, the company operates in the utilities industry, with a strong focus on three segments, namely Water, Recycling and Recovery, Environmental Technologies and Solutions. This strategy is supported by a lean corporate structure, which defines resource allocation and organizes technical expertise. The company was originally an operating division of Suez, and it was only after the 2008 merger, which created GDF Suez (currently Engie S.A.), that it was separated as a stand-alone entity. After the IPO of the same year, Suez Environment’ shares skyrocketed reaching 40% in value on the very first day. In July 2015, after the group GDF Suez changed its name to Engie, the brand Suez Environment was simplified to simply Suez. Moreover, in September of the same year, it acquired a 40% stake in Sembcorp to provide water and waste management in Australia and in October 2017 it bought the Water & Process Technologies unit from GE Power, thus forming the new Water Technologies & Solutions business unit.

Until recent events, Engie, a French multinational company and global provider of electricity, gas and associated energy and environment services throughout the world, has been the largest shareholder of Suez, with an almost 35% stake (which in 2020 was sold to Veolia). Other major shareholders include Criteria Caixa (6%), Inversiones Los Canelos (3.6%) and Caltagirone Group (3.5%). Moreover, 51.8% of the total shares of the company are free float.

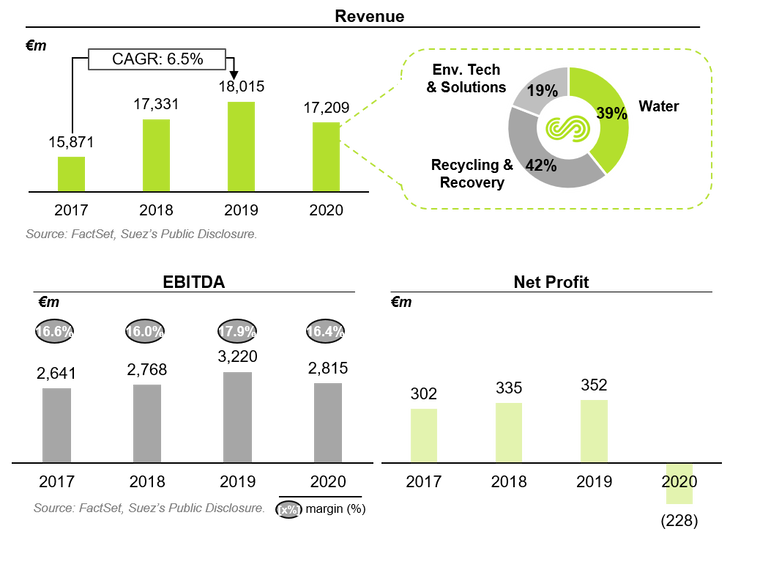

Prior to the pandemic, Suez managed to demonstrate organic growth in all business sectors with Recycling & Recovery and Water businesses being the main revenue-level contributors. At the same time, the company demonstrated commitment towards the Environmental Tech & Solutions business by increasing CAPEX dedicated to this business sector, resulting in the accelerated growth in this segment (~7.0% compared to ~2.9% of R&R and Water). Suez also managed to maintain a sustainable profitability level, even despite being under financial pressure due to the extraordinary acquisition costs of GE Water. Despite the negative effect of COVID-19 in H1 2020, the company managed to partially recover during H2 2020, even exceeding initial guidance. Even during the pandemic, Suez managed to continue to implement its strategic plan by focusing on environmental solutions and divestiture of non-core assets. In 2021, the company expects to fully recover from the negative effects of the pandemic and return to the pre-pandemic level of financial performance.

Strong financial results in H2 2020 and management confidence about the future financial performance of the company serve as one of the main arguments for undervaluation of the company in Veolia’s offer.

Veolia

Veolia Environnement S.A., commonly known as Veolia, is a multinational corporation based in Paris, France. Its mission is to help cities and industries around the globe to efficiently manage their resources, thus promoting the development and protection of the environment. In order to reach this goal, it offers innovative solutions that are mainly focused on three business activities: water management, waste management and energy services. The company’s history dates back to 1853 when a water company named Compagnie Générale des Eaux (CGE) was formed by an imperial decree of Napoleon III. After more than a century, in 1998, CGE changed its name to Vivendi and sold off its property and construction divisions. The following year, Vivendi Environnement was formed to consolidate its environmental divisions: the company went public on the NYSE in December 1999, and soon after it announced a merger with Canal+ and Seagram to become Vivendi Universal, now Vivendi. In July 2000, Vivendi Environnement was divested through an IPO, thus becoming a stand-alone entity in which initially Vivendi Universal’ stake was 70%, but it was reduced to 20.4% by December 2002. In 2003, Vivendi Environnement was renamed to Veolia Environnement.

Although Veolia and Suez have similar corporate structures and converging operational strategies, Veolia is relatively larger compared to Suez from a revenues’ viewpoint.

Strong financial results in H2 2020 and management confidence about the future financial performance of the company serve as one of the main arguments for undervaluation of the company in Veolia’s offer.

Veolia

Veolia Environnement S.A., commonly known as Veolia, is a multinational corporation based in Paris, France. Its mission is to help cities and industries around the globe to efficiently manage their resources, thus promoting the development and protection of the environment. In order to reach this goal, it offers innovative solutions that are mainly focused on three business activities: water management, waste management and energy services. The company’s history dates back to 1853 when a water company named Compagnie Générale des Eaux (CGE) was formed by an imperial decree of Napoleon III. After more than a century, in 1998, CGE changed its name to Vivendi and sold off its property and construction divisions. The following year, Vivendi Environnement was formed to consolidate its environmental divisions: the company went public on the NYSE in December 1999, and soon after it announced a merger with Canal+ and Seagram to become Vivendi Universal, now Vivendi. In July 2000, Vivendi Environnement was divested through an IPO, thus becoming a stand-alone entity in which initially Vivendi Universal’ stake was 70%, but it was reduced to 20.4% by December 2002. In 2003, Vivendi Environnement was renamed to Veolia Environnement.

Although Veolia and Suez have similar corporate structures and converging operational strategies, Veolia is relatively larger compared to Suez from a revenues’ viewpoint.

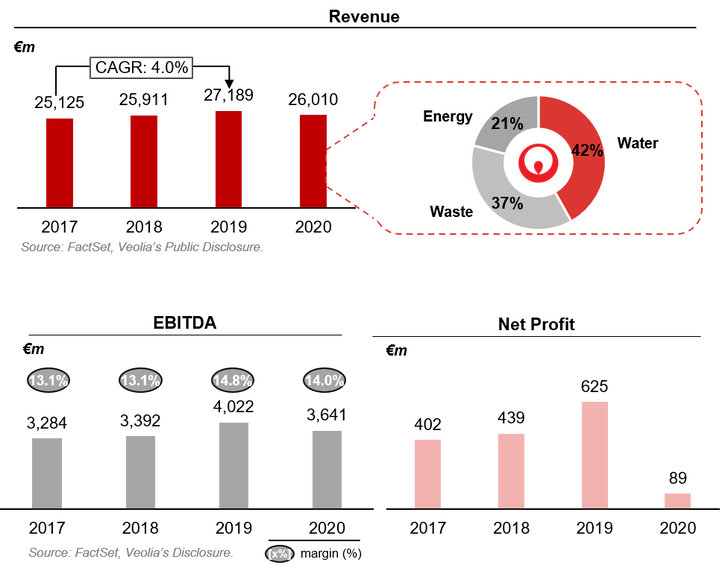

Prior to the pandemic, Veolia managed to demonstrate solid financial performance by increasing its revenue base and at the same time managing to improve efficiency through the implementation of cost-saving programs. Despite the negative effect of the COVID-19 pandemic, Veolia managed to achieve its main strategic goals and preserve financial robustness. In 2021, the company expects to fully recover from the negative effects of the pandemic and return to the pre-pandemic level of financial performance.

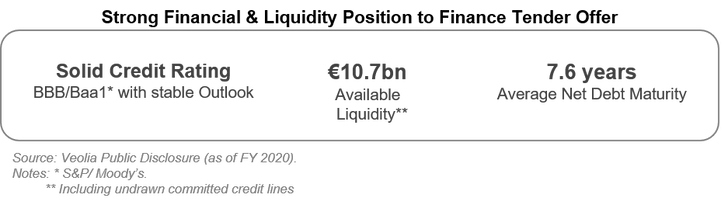

At the same time, Suez managed to maintain strong liquidity position to finance future potential acquisitions. Despite the volatility in the market during 2020, the company managed to raise additional ~€3.7bn in debt financing, increasing resources at deposition and refinancing existing debt at better conditions.

At the same time, Suez managed to maintain strong liquidity position to finance future potential acquisitions. Despite the volatility in the market during 2020, the company managed to raise additional ~€3.7bn in debt financing, increasing resources at deposition and refinancing existing debt at better conditions.

Ardian

Ardian, formerly Axa private equity, is a French private equity investment company founded by Dominique Senequier and one of the largest European private equity funds. Their mission is to help troubled firms with talented management teams to achieve sustainable and long-term value, as well as the positive social impact that would benefit all company’s shareholders. Ardian manages $110bn assets across the globe on behalf of governments, institutions, pension funds and high net-worth individuals and it does so through trusting and long-term partnerships developed with more than 1,000 investors in more than 50 countries.

Deal Rationale

Veolia x Suez

On 5th October 2020, Veolia bought 29.9% of the share capital and voting rights of Suez from Engie to develop an ambitious program aiming at constructing a major leading player in the ecological transformation industry. The selling player, Engie, opted for Veolia as the buying partner that offered the most attractive offer and guaranteed a solid commitment for future projects. Veolia’s ultimate objective is then to acquire the residual shares of Suez to complete a final takeover bid set at €18 per share that would bring synergies and concrete benefits for all the shareholders involved.

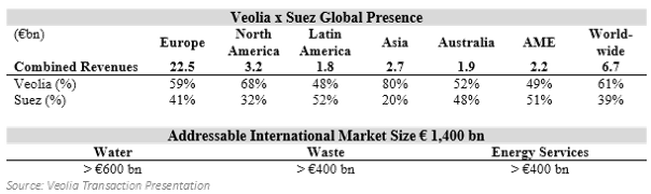

The underlying motives leading the business combination are mainly referred to as the intention to create a global ecological firm grounded on the complementarity of established French and European roots and to target a potential expansion in growth markets in the Americas and Asia. Since the ecological transformation sector is experiencing slow growth and considerable fragmentation, the merger would enable an aggregation of forces and expertise that would lead to a 5% global market share.

Ardian, formerly Axa private equity, is a French private equity investment company founded by Dominique Senequier and one of the largest European private equity funds. Their mission is to help troubled firms with talented management teams to achieve sustainable and long-term value, as well as the positive social impact that would benefit all company’s shareholders. Ardian manages $110bn assets across the globe on behalf of governments, institutions, pension funds and high net-worth individuals and it does so through trusting and long-term partnerships developed with more than 1,000 investors in more than 50 countries.

Deal Rationale

Veolia x Suez

On 5th October 2020, Veolia bought 29.9% of the share capital and voting rights of Suez from Engie to develop an ambitious program aiming at constructing a major leading player in the ecological transformation industry. The selling player, Engie, opted for Veolia as the buying partner that offered the most attractive offer and guaranteed a solid commitment for future projects. Veolia’s ultimate objective is then to acquire the residual shares of Suez to complete a final takeover bid set at €18 per share that would bring synergies and concrete benefits for all the shareholders involved.

The underlying motives leading the business combination are mainly referred to as the intention to create a global ecological firm grounded on the complementarity of established French and European roots and to target a potential expansion in growth markets in the Americas and Asia. Since the ecological transformation sector is experiencing slow growth and considerable fragmentation, the merger would enable an aggregation of forces and expertise that would lead to a 5% global market share.

The merger between the two entities would allow to create the world champion for ecological transformation, which would be in line with the European Commission objectives and further green incentive packages. The strategic and cultural overlap between Veolia and Suez represents a clear signal for a successful integration that could lead the group to become the primary player for the EU Green Deal, focusing on challenging green projects in water treatment, alternative clean energy developments, new pollution treatment solutions, RDF and several others energy-related projects such as lithium battery recycling or waste heat recovery.

Hence, the unification of the two entities would create value for various stakeholders and would benefit from the strong complementarities in geographical as well as technological and client portfolio aspects, that are conducive for global value creation. The combination would amplify the innovation capabilities and investments that are needed to develop technologies needed to succeed in the green transformation.

Veolia’s strategic plan for 2023 and Suez’s strategic objectives for 2030 appear to be tremendously aligned toward the common direction to become the global leader in ecological transformation, to expand overseas and to improve in profitability and efficiencies. Hence, the strategic fit and complementarity of assets will make the firms’ integration highly likely to succeed and to pursue common objectives as a distinctive and stronger entity.

Moreover, the combination embodies a unique opportunity for their clients to move quickly towards environmental efficiency. For instance, the combined unique expertise in water, waste and energy technologies would allow the diverse pool of customers, namely municipal, industrial, tertiary and others, to accelerate towards the environmental transformation.

Hence, the unification of the two entities would create value for various stakeholders and would benefit from the strong complementarities in geographical as well as technological and client portfolio aspects, that are conducive for global value creation. The combination would amplify the innovation capabilities and investments that are needed to develop technologies needed to succeed in the green transformation.

Veolia’s strategic plan for 2023 and Suez’s strategic objectives for 2030 appear to be tremendously aligned toward the common direction to become the global leader in ecological transformation, to expand overseas and to improve in profitability and efficiencies. Hence, the strategic fit and complementarity of assets will make the firms’ integration highly likely to succeed and to pursue common objectives as a distinctive and stronger entity.

Moreover, the combination embodies a unique opportunity for their clients to move quickly towards environmental efficiency. For instance, the combined unique expertise in water, waste and energy technologies would allow the diverse pool of customers, namely municipal, industrial, tertiary and others, to accelerate towards the environmental transformation.

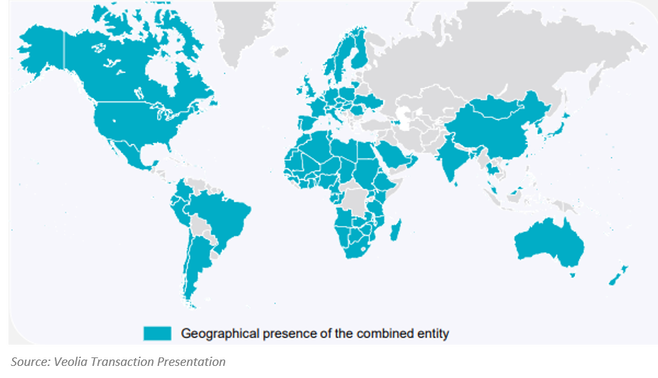

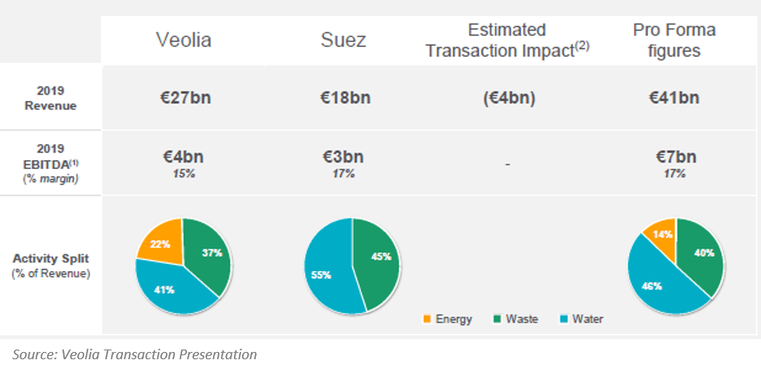

Furthermore, the merged group would tend to expand its global footprint and increase in size, reaching approximatively €40bn of annual revenues, as well as roughly €7bn of EBITDA, keeping a high-level of EBITDA margin at 17%. Not only would it expand in dimension, but it would also spread internationally, 24% in France, 34% in the rest of Europe and would try to expand in growth markets in Asia and Latin America.

According to the projections, the merger will generate €300m of operational synergies and €200m of purchasing synergies, amounting to a total of approximatively €500m, fully achieved within a time frame of four years, 20% of which already in the first year.

As for shareholders, the transaction would entail accretive EPS from the first year and high double-digit from the third year onwards after the closing, while still preserving financial soundness and a strong investment-grade rating.

According to the projections, the merger will generate €300m of operational synergies and €200m of purchasing synergies, amounting to a total of approximatively €500m, fully achieved within a time frame of four years, 20% of which already in the first year.

As for shareholders, the transaction would entail accretive EPS from the first year and high double-digit from the third year onwards after the closing, while still preserving financial soundness and a strong investment-grade rating.

Ardian and GIP Rationale (supported by Suez BoD)

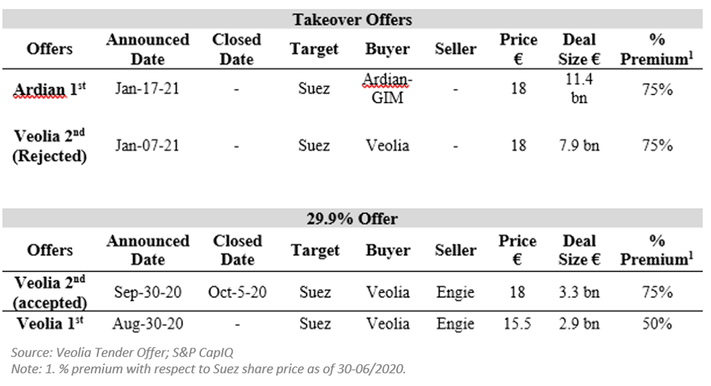

Besides Veolia’s takeover bid proposal, on January 17th 2021 private equity investors Ardian and Global Infrastructure Partners made an alternative bid to acquire Veolia’s 29.9% and remaining shares of Suez for €11.7bn. The bid is set at €18 per share and the proposal would involve the preservation of the workforce and keep the competition within France. Veolia stated that their 29.9% stake in Suez is not and will not be for sale and would deem hostile any proposal concerning a sale or transfer that would prevent its efforts to acquire Suez. However, as said by the head of Ardian Infrastructure, Mathias Burghardt, the LOI was not meant to be an alternative to Veolia’s offer, but rather a way “to allow a negotiation to take place”, which depends on a potential agreement between Veolia and Suez. Suez BoD supported the takeover bid by Ardian and GIP, which could be seen as a white knight proposal against Veolia’s hostile takeover (a white knight is a protection mechanism that involves a friendly company to acquire the target, which would otherwise be taken over by an unfriendly bidder, the black knight). The strategic move taken by the partnership of Ardian and GIP comes as a responsible investment aimed at avoiding the dismantle of Suez and trying to find a quick and friendly solution between the two environmental players for the best interests of all the stakeholders.

The Conflict

Since the initial offer handed by Veolia at the end of August 2020, the management of the target company has experienced a conflicting relationship with Veolia and has set up a series of constraints that are limiting the buyer from proceeding with the takeover process. Since the preliminary approach, Suez’s CEO, Mr. Camus, has refused to engage in a constructive discussion with Mr. Frerot, CEO of Veolia. The management of Suez pursued a destructive strategy structuring a poison pill in September 2020 that would prevent takeovers or changes of control (poison pills refer to deliberate tactics, namely flip-in or flip-over strategies, undertaken by the target to discourage potential buyers and prevent hostile takeovers). In particular, Suez moved its French water assets to a Dutch vehicle that is meant to secure them until Suez’s BoD decides otherwise. As a result, a tight legal battle has taken place between the two parties, since Veolia questioned the poison pill to be illegal and void. The hostility brought by Suez BoD irritated Veolia’s CEO Mr Frérot that told the Financial Times: “The current board is refusing to start a dialogue, so, if it refuses up until the very end, this will be done with another board. But our project . . . it will be completed.”

Suez CEO Mr. Camus welcomed the proposal by Ardian and GIP as an offer that would prevent concerns over jobs and anti-trust issues, unlike Veolia’s bid, stating that “It’s the implementation of a friendly solution... with scenarios that could be different, but that could lead to an offer for all of it”. According to people close to Suez, Veolia’s CEO, Mr Frérot, left a door open for a possible carve-out of the French water business of Suez, amounting to roughly €5bn of revenues a year, that would be handled by the on-going administration. However, Suez declined the proposal, fearing that a business mostly restricted to French water would not be able to remain significant. As an alternative Veolia could opt for accepting some assets from Suez’s portfolio giving up the takeover walking away.

According to Suez’s chief executive Mr. Camus: “Suez in the future has to have a coherent industrial project. It has to be a company that can grow, that can compete in the market. It cannot be just a sum of things that cannot be kept by Veolia”. Recent rumours suggest the possibility of an opening to negotiations to finally find a solution to the tumultuous occurrences.

Latest Developments

As of 8th February 2021, Suez challenged the validity of Veolia’s tender offer to the Commercial Court of Nanterre that ordered Veolia to suspend the launch of the operation, pending a substantive debate on its previous amicable settlement commitments. The transaction has been so controversial in France that the Minister of the Economy Bruno Le Maire intervened saying that he would ask the AMF, the French financial market regulator, to deal with the situation, as Veolia’s offer appeared not to be friendly and to violate the previous commitments. However, on February 11th 2021, the Paris Court of Appeal dismissed Suez claims and validated the rights of Veolia, which is therefore legally entitled to continue with the takeover efforts. The latest events demonstrate a series of court victories for Veolia, which is now pressing Suez to be more proactive and open to finding a friendly solution. Veolia’s management believes the destructive tactics exhibited by Suez are menacing market integrity and in case an agreement would not be found soon, shareholders should be entitled to make their voices heard and decide on the tender offer at a general meeting.

On 26th February 2021 Board of Directors of Suez unanimously rejected Veolia’s takeover offer, formalizing opposition to the bid. The main arguments were that the price offered by Veolia did not reflect the true value created by Suez and the offer would threaten corporate interests by dismantling the firm and providing unsatisfactory job guarantees, only limited to a certain period of time. The situation still remains unclear due to Veolia’s significant ownership in Suez and its determination to complete the deal, therefore further developments can be fir sure expected.

In the beginning of March, Veolia announced that they are going to make another (improved) offer and hope to reach a positive outcome in the situation.

Deals Structure

On 30th August 2020 Veolia offered to purchase 29.9% of Engie’s stake in Suez for €2.9bn at €15.5 per share (cum dividend). The offer entailed a significant 49% premium on unaffected 3-month VWAP and 50% on 30 July 2020 closing price, giving substantial value realization to Suez’s shareholders and was valid until 30th September 2020. Later Veolia raised an offer of €3.3bn at €18 per share (cum dividend) on 30th September 2020, which was accepted by the BoD of Engie on 5th October 2020.

On 7th January 2021, Veolia issued a takeover bid for all the remaining Suez’s shareholders, 70.1% for €7.9bn, upholding the same transparent terms offered for the 29.9% stake in Engie, thus €18 per share cum dividend. The offer price constitutes the highest share price in the last five years and it had a 8.4% premium with respect to the closing market price one day prior to the announcement. In addition, the offer price presented by Veolia amounts to 33.1x NTM earnings and 1.9x forward book value. The bid will be invalidated if Veolia fails to buy more than 50% of Suez capital. The transaction is expected to terminate in the first quarter of 2022, with the closing of the offer estimated to occur on 19th April 2022.

The overall amount of all costs, fees and expenses related to the takeover offer, financial, legal, accounting advisors fees and other linked costs, amounts to roughly €150m (excluding taxes). If the takeover goes as expected, the maximum cost of the offer will aggregate to nearly €7.95bn. The transaction will be covered by a bridge loan through a bank pool. The loan would be refinanced partly by the proceeds of the disposals required by the competition authorities and partly by the issuance of hybrid bonds and of share capital securities or securities giving access to the share capital, in order to preserve a robust investment grade rating and to keep the net financial Debt/EBITDA ratio of the combined group below 3.0x in the medium term.

Offers Overview

Besides Veolia’s takeover bid proposal, on January 17th 2021 private equity investors Ardian and Global Infrastructure Partners made an alternative bid to acquire Veolia’s 29.9% and remaining shares of Suez for €11.7bn. The bid is set at €18 per share and the proposal would involve the preservation of the workforce and keep the competition within France. Veolia stated that their 29.9% stake in Suez is not and will not be for sale and would deem hostile any proposal concerning a sale or transfer that would prevent its efforts to acquire Suez. However, as said by the head of Ardian Infrastructure, Mathias Burghardt, the LOI was not meant to be an alternative to Veolia’s offer, but rather a way “to allow a negotiation to take place”, which depends on a potential agreement between Veolia and Suez. Suez BoD supported the takeover bid by Ardian and GIP, which could be seen as a white knight proposal against Veolia’s hostile takeover (a white knight is a protection mechanism that involves a friendly company to acquire the target, which would otherwise be taken over by an unfriendly bidder, the black knight). The strategic move taken by the partnership of Ardian and GIP comes as a responsible investment aimed at avoiding the dismantle of Suez and trying to find a quick and friendly solution between the two environmental players for the best interests of all the stakeholders.

The Conflict

Since the initial offer handed by Veolia at the end of August 2020, the management of the target company has experienced a conflicting relationship with Veolia and has set up a series of constraints that are limiting the buyer from proceeding with the takeover process. Since the preliminary approach, Suez’s CEO, Mr. Camus, has refused to engage in a constructive discussion with Mr. Frerot, CEO of Veolia. The management of Suez pursued a destructive strategy structuring a poison pill in September 2020 that would prevent takeovers or changes of control (poison pills refer to deliberate tactics, namely flip-in or flip-over strategies, undertaken by the target to discourage potential buyers and prevent hostile takeovers). In particular, Suez moved its French water assets to a Dutch vehicle that is meant to secure them until Suez’s BoD decides otherwise. As a result, a tight legal battle has taken place between the two parties, since Veolia questioned the poison pill to be illegal and void. The hostility brought by Suez BoD irritated Veolia’s CEO Mr Frérot that told the Financial Times: “The current board is refusing to start a dialogue, so, if it refuses up until the very end, this will be done with another board. But our project . . . it will be completed.”

Suez CEO Mr. Camus welcomed the proposal by Ardian and GIP as an offer that would prevent concerns over jobs and anti-trust issues, unlike Veolia’s bid, stating that “It’s the implementation of a friendly solution... with scenarios that could be different, but that could lead to an offer for all of it”. According to people close to Suez, Veolia’s CEO, Mr Frérot, left a door open for a possible carve-out of the French water business of Suez, amounting to roughly €5bn of revenues a year, that would be handled by the on-going administration. However, Suez declined the proposal, fearing that a business mostly restricted to French water would not be able to remain significant. As an alternative Veolia could opt for accepting some assets from Suez’s portfolio giving up the takeover walking away.

According to Suez’s chief executive Mr. Camus: “Suez in the future has to have a coherent industrial project. It has to be a company that can grow, that can compete in the market. It cannot be just a sum of things that cannot be kept by Veolia”. Recent rumours suggest the possibility of an opening to negotiations to finally find a solution to the tumultuous occurrences.

Latest Developments

As of 8th February 2021, Suez challenged the validity of Veolia’s tender offer to the Commercial Court of Nanterre that ordered Veolia to suspend the launch of the operation, pending a substantive debate on its previous amicable settlement commitments. The transaction has been so controversial in France that the Minister of the Economy Bruno Le Maire intervened saying that he would ask the AMF, the French financial market regulator, to deal with the situation, as Veolia’s offer appeared not to be friendly and to violate the previous commitments. However, on February 11th 2021, the Paris Court of Appeal dismissed Suez claims and validated the rights of Veolia, which is therefore legally entitled to continue with the takeover efforts. The latest events demonstrate a series of court victories for Veolia, which is now pressing Suez to be more proactive and open to finding a friendly solution. Veolia’s management believes the destructive tactics exhibited by Suez are menacing market integrity and in case an agreement would not be found soon, shareholders should be entitled to make their voices heard and decide on the tender offer at a general meeting.

On 26th February 2021 Board of Directors of Suez unanimously rejected Veolia’s takeover offer, formalizing opposition to the bid. The main arguments were that the price offered by Veolia did not reflect the true value created by Suez and the offer would threaten corporate interests by dismantling the firm and providing unsatisfactory job guarantees, only limited to a certain period of time. The situation still remains unclear due to Veolia’s significant ownership in Suez and its determination to complete the deal, therefore further developments can be fir sure expected.

In the beginning of March, Veolia announced that they are going to make another (improved) offer and hope to reach a positive outcome in the situation.

Deals Structure

On 30th August 2020 Veolia offered to purchase 29.9% of Engie’s stake in Suez for €2.9bn at €15.5 per share (cum dividend). The offer entailed a significant 49% premium on unaffected 3-month VWAP and 50% on 30 July 2020 closing price, giving substantial value realization to Suez’s shareholders and was valid until 30th September 2020. Later Veolia raised an offer of €3.3bn at €18 per share (cum dividend) on 30th September 2020, which was accepted by the BoD of Engie on 5th October 2020.

On 7th January 2021, Veolia issued a takeover bid for all the remaining Suez’s shareholders, 70.1% for €7.9bn, upholding the same transparent terms offered for the 29.9% stake in Engie, thus €18 per share cum dividend. The offer price constitutes the highest share price in the last five years and it had a 8.4% premium with respect to the closing market price one day prior to the announcement. In addition, the offer price presented by Veolia amounts to 33.1x NTM earnings and 1.9x forward book value. The bid will be invalidated if Veolia fails to buy more than 50% of Suez capital. The transaction is expected to terminate in the first quarter of 2022, with the closing of the offer estimated to occur on 19th April 2022.

The overall amount of all costs, fees and expenses related to the takeover offer, financial, legal, accounting advisors fees and other linked costs, amounts to roughly €150m (excluding taxes). If the takeover goes as expected, the maximum cost of the offer will aggregate to nearly €7.95bn. The transaction will be covered by a bridge loan through a bank pool. The loan would be refinanced partly by the proceeds of the disposals required by the competition authorities and partly by the issuance of hybrid bonds and of share capital securities or securities giving access to the share capital, in order to preserve a robust investment grade rating and to keep the net financial Debt/EBITDA ratio of the combined group below 3.0x in the medium term.

Offers Overview

Market Reaction

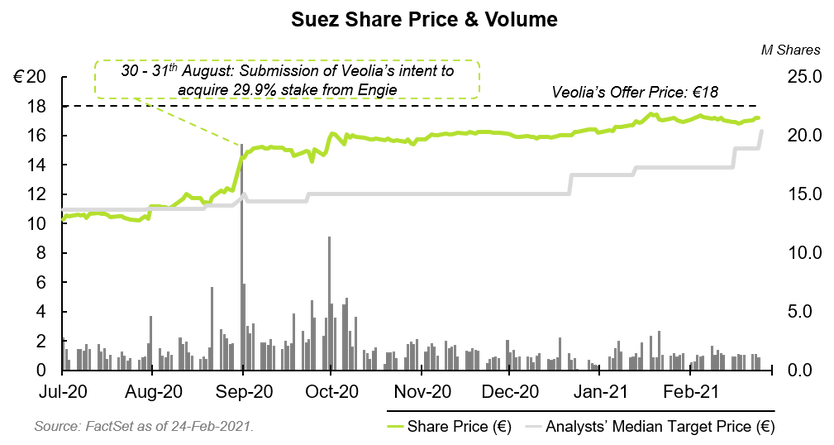

The first remarkable shock to Suez’s share price was seen on 31st July 2020, the day of Engie’s announcement that Veolia would acquire 29.9% share from them: Suez’s shares gained almost 8.7% (to the previous day). The share price has since then risen constantly, but the most significant shock was registered when Veolia’s proposal was officially submitted at the end of August, with Suez’s share price hitting a record of €14.5 per share. However, it was only on October 5th that Veolia formally acquired the previously established block of Suez from Engie at a price of € 18 per share (dividend included) and presented the intention to file a voluntary takeover bid for the remaining Suez capital. As a consequence, the day after the completion of the acquisition, Suez shares rose up to € 16.1.

Due to Suez implementing anti-takeover tactics share price was fluctuating below Veolia’s offer demonstrating market uncertainty regarding the successful outcome of the potential takeover. However, from the beginning/mid-December 2020, share price, as well as analysts’ median target, demonstrated an upward trend signalling positive movements in relation to the legal approvals of the launch of the tender offer. Starting from mid-February 2021 due to the positive outcomes of processual hearings, analysts continuously raised their target prices almost reaching the market level. As of the end of February, both actual and target share prices have almost converged to Veolia’s offer price, demonstrating market confidence regarding the eventual approval and successful launch of the tender offer.

Due to Suez implementing anti-takeover tactics share price was fluctuating below Veolia’s offer demonstrating market uncertainty regarding the successful outcome of the potential takeover. However, from the beginning/mid-December 2020, share price, as well as analysts’ median target, demonstrated an upward trend signalling positive movements in relation to the legal approvals of the launch of the tender offer. Starting from mid-February 2021 due to the positive outcomes of processual hearings, analysts continuously raised their target prices almost reaching the market level. As of the end of February, both actual and target share prices have almost converged to Veolia’s offer price, demonstrating market confidence regarding the eventual approval and successful launch of the tender offer.

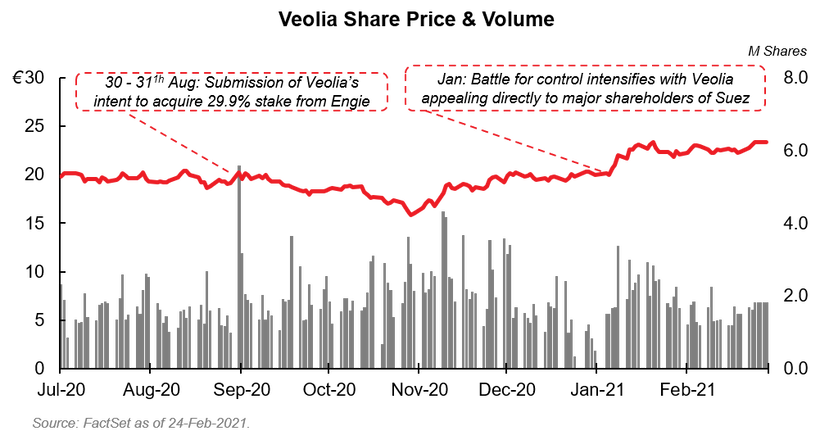

On 31st August 2020, the day after the initial announcement of Veolia’s intention to acquire 29.9% of Suez from Engie, Veolia’s share price rose to € 20.2, gaining almost 5.6% with respect to the previous day. After the deal was concluded at the beginning of October, and Veolia confirming its intention to acquire full control over Suez, the market reacted with downward expectations on Veolia share price at the end of October. This was mainly due to the French Court of Appeals concluding that Veolia must have consulted unions before proceeding with 29.9% Suez purchase, which added more complexity and uncertainty to the deal resulting in the share price hitting a low of € 15.85 on Oct 29th. Nevertheless, by the beginning of November Veolia stated in a statement that the ruling of the Court was unlikely to delay its plan to take full control of Suez, which made share price recover very quickly. After some volatility until year-end due to Suez trying to find some ways to avoid the takeover, the battle with Veolia intensified at the beginning of January 2021, with Veolia CEO Antoine Frerot deciding to appeal directly to Suez’s shareholders due to the impossibility to expose its project to Suez’s Board. The latest positive shock to Veolia share price in mid-January clearly shows investors’ confidence in Veolia succeeding in its plan of acquisition of full control.

Advisors

In the on-going process Veolia is advised by Perella Weinberg, Messier Maris and Citi, while Goldman Sachs, JPMorgan, Société Générale and Rothschild are working for Suez.

BSCM would like to thank FactSet for giving us access to their platform and providing charts and data.

Annamaria Palmieri

Natalia Szperna

Paolo Taveggia

Want to keep up with our most recent articles? Subscribe to our weekly newsletter here.

Sources:

Advisors

In the on-going process Veolia is advised by Perella Weinberg, Messier Maris and Citi, while Goldman Sachs, JPMorgan, Société Générale and Rothschild are working for Suez.

BSCM would like to thank FactSet for giving us access to their platform and providing charts and data.

Annamaria Palmieri

Natalia Szperna

Paolo Taveggia

Want to keep up with our most recent articles? Subscribe to our weekly newsletter here.

Sources:

- FactSet

- S&P CapIQ

- Veolia public disclosure

- Suez public disclosure

- Ardian Public disclosure

- OPEC (World Oil Outlook 2045)

- International Energy Agency

- World Bank

- UN (UN World Water development report 2019)

- FT

- Reuters