Natural gas prices are skyrocketing around the world

In recent times, following the global health crisis of Covid-19, natural gas prices on continental Europe have reached levels not seen for years. This trend has been caused by a combination of factors which will be discussed in detail in the following paragraphs. Indeed, incredibly high gas prices are related to the nature of the product, its usefulness and weather but also to Covid-19 consequences and to political patterns. Moreover, it is also important to consider how this phenomenon will affect the European economy and financial markets.

Market overview and focus on Europe

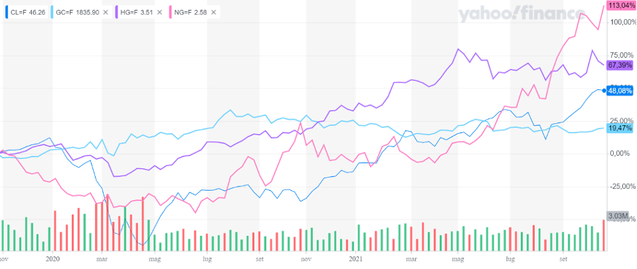

Starting from considering the situation of the market of commodities, observing DJ Commodities Index, it is noticeable that different groups of commodities have shown an increase in futures price. Considering metals, in the last year copper has risen by 67% and in the last semester fluctuated but still remained above $4.1, which is 33% higher than the previous October. Similar trend for gold and silver. The strong rise in natural gas futures price has started in the first semester of 2021, reaching a price of $5.619 in September which is double compared to the one of previous year. Other commodities related to energy, such as oil, copper and coal, are following a similar trend. Natural gas showed a significant decrease in the last weeks of October after Putin’s announcement of starting to fill storage facilities from November onwards. Taking into account fuels, Crude oil started a sharp increase after April 2020 (when futures prices became negative (with a minimum of -$40.32) for the first time as a consequence of Covid restrictions for transports and travelling) and it overcame $80 per barrel in October 2021. Also Brent oil showed a similar pattern, but remaining positive. Coal reached a peak in October 2021 after quite a year of strong increase and in November it steadily decreased. Probably this trend is strongly correlated with the strong increase in natural gas that incentives switching to the use of coal rather than natural gas to produce electricity. Main worries about this situation is the fact that the surge of energy prices may accelerate the increase of global inflation and influence policy choice. Considering the point of view of investors, they started to use the term “commodity supercycle” to describe the current movements. A commodity supercycle is a structural change in the value of prices that can last decades. Anyway, according to numerous economists the only commodities that may enter in this cycle is coal, due to switching from fossil fuel to electric solutions.

In recent times, following the global health crisis of Covid-19, natural gas prices on continental Europe have reached levels not seen for years. This trend has been caused by a combination of factors which will be discussed in detail in the following paragraphs. Indeed, incredibly high gas prices are related to the nature of the product, its usefulness and weather but also to Covid-19 consequences and to political patterns. Moreover, it is also important to consider how this phenomenon will affect the European economy and financial markets.

Market overview and focus on Europe

Starting from considering the situation of the market of commodities, observing DJ Commodities Index, it is noticeable that different groups of commodities have shown an increase in futures price. Considering metals, in the last year copper has risen by 67% and in the last semester fluctuated but still remained above $4.1, which is 33% higher than the previous October. Similar trend for gold and silver. The strong rise in natural gas futures price has started in the first semester of 2021, reaching a price of $5.619 in September which is double compared to the one of previous year. Other commodities related to energy, such as oil, copper and coal, are following a similar trend. Natural gas showed a significant decrease in the last weeks of October after Putin’s announcement of starting to fill storage facilities from November onwards. Taking into account fuels, Crude oil started a sharp increase after April 2020 (when futures prices became negative (with a minimum of -$40.32) for the first time as a consequence of Covid restrictions for transports and travelling) and it overcame $80 per barrel in October 2021. Also Brent oil showed a similar pattern, but remaining positive. Coal reached a peak in October 2021 after quite a year of strong increase and in November it steadily decreased. Probably this trend is strongly correlated with the strong increase in natural gas that incentives switching to the use of coal rather than natural gas to produce electricity. Main worries about this situation is the fact that the surge of energy prices may accelerate the increase of global inflation and influence policy choice. Considering the point of view of investors, they started to use the term “commodity supercycle” to describe the current movements. A commodity supercycle is a structural change in the value of prices that can last decades. Anyway, according to numerous economists the only commodities that may enter in this cycle is coal, due to switching from fossil fuel to electric solutions.

Figure 1: Commodities prices (YOY % change). Note: GC= Gold, HG=Copper, CL=Crude oil, NG=Natural Gas. Source: Yahoo Finance

Figure 2: Gas prices tumble in Europe as Russia signals more supplies next month. Source: Financial Times

Now the analysis proceeds focusing on the peculiar trend for natural gas futures price.

How is natural gas affecting electricity prices?

The impact of the natural gas price rise on households and industry passes also through the increase in the cost of electricity, and this impacts European citizens especially due to the price setting mechanism through which the electricity price is determined. Before the 1990’s, the electricity supply of single member states was regulated by national monopolies, which were characterized by significant vertical integration in the electricity market given that they provided for distribution, transmission and retail of electricity. The introduction of several European directives encouraged to gradually open these markets to competition, for example by leaving retail energy to private companies and by encouraging coupling of electricity markets between countries. Although a unique European energy market still has to be developed, organized international electricity markets exist between countries through the “market coupling” mechanism, involving interconnectors which transport energy across borders. An example is the European Power exchange (EPEX) which involves 13 European countries and which allows each country to cover its need for electricity by acquiring the excess capacity of other countries. Alternatively to energy markets selling standard products, countries can exchange energy through over the counter markets.

International electricity markets involve the exchange of long term derivatives such as options to hedge price volatility, or short term spot markets such as the day-ahead market and the intraday market. In the day-ahead market, suppliers specify quantities and minimum prices they are willing to accept and buyers pose bids with required quantities and maximum prices they are willing to pay. The price for each hour of the successive day is determined in an auction closing at 12AM by intersecting demand and supply curves, and taking into account the cross-border transmission constraint. As a result, the marginal price of electricity at which buyers and sellers are willing to exchange the quantity available becomes the electricity price paid by all. This pay as clear system implies that all the suppliers' offers are sorted by increasing price and those who are willing to accept less than the market price will sell their energy at the higher equilibrium market price, while the opposite happens with regards to buyers. This market system incentivizes suppliers to offer their product at their marginal cost of production, composed of the fuel cost, the start-up cost and the cost for emission allowances, given that receiving any price above this marginal cost would allow them to pay for their fixed costs as well. The second type of market countries engage in is the intraday market, where market participants trade continuously with delivery on the same day, in order to balance their electricity positions in response to oscillations in demand and production supply, closer to the time at which they are required. The fact that energy produced by renewables is sold at a lower marginal cost, given the absence of fuel and emission allowances cost, means that all renewable energy produced is exchanged before any other energy type. This is particularly useful given that renewable energy production is intermittent, characterized by large oscillations in power produced and is almost impossible to store. The size of the market demand, oscillating between 218 and 277 Giga Watt hour per month in 2019, however, makes it necessary that non renewable energy sources such as natural gas and coal are used to clear the market, meaning that electricity price is heavily dependent on the price of these prime commodities. This is demonstrated in the rising electricity prices today, due to the raise in natural gas prices.

Why is this happening

It is fair to say that the recent surge in natural gas prices is not the consequence of an individual “shock event” on the demand or supply side of the global natural gas market. In reality, there are multiple reasons for which Europe as well as many other parts of the globe are experiencing such fluctuations in the price of natural gas.

The Resurgence of Consumer Demand Post Covid

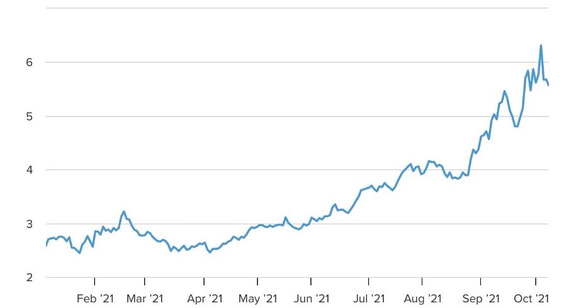

During the depths of the coronavirus pandemic, demand for goods and services fell as global savers managed to amass an additional $5.4tn (6% of Global GDP) according to figures published by credit rating agency Moody’s. Nevertheless, following the last two gruelling years of endless lockdowns, these consumer habits have been short lived. What must be said is that the global economic recovery has been much faster than expected as restrictions have been dropped in the vast majority of European nations (including the UK). For example, household marginal propensity to consume has risen at levels never seen before. This has been shown in Europe as GDP is expected to grow by 4.8% in euro-bearing countries over 2021 (according to the European Commission) and by 6.5% in the UK according to Rishi Sunday (The Chancellor of the Exchequer in the UK). These increases have correlated strongly with the increasing global gas demand of 3.6% (according to the IEA) as consumer spending for goods and services requiring natural gas (heating, refrigeration and hot water) has increased rapidly. As demand has increased, the price of natural gas has increased as shown below:

How is natural gas affecting electricity prices?

The impact of the natural gas price rise on households and industry passes also through the increase in the cost of electricity, and this impacts European citizens especially due to the price setting mechanism through which the electricity price is determined. Before the 1990’s, the electricity supply of single member states was regulated by national monopolies, which were characterized by significant vertical integration in the electricity market given that they provided for distribution, transmission and retail of electricity. The introduction of several European directives encouraged to gradually open these markets to competition, for example by leaving retail energy to private companies and by encouraging coupling of electricity markets between countries. Although a unique European energy market still has to be developed, organized international electricity markets exist between countries through the “market coupling” mechanism, involving interconnectors which transport energy across borders. An example is the European Power exchange (EPEX) which involves 13 European countries and which allows each country to cover its need for electricity by acquiring the excess capacity of other countries. Alternatively to energy markets selling standard products, countries can exchange energy through over the counter markets.

International electricity markets involve the exchange of long term derivatives such as options to hedge price volatility, or short term spot markets such as the day-ahead market and the intraday market. In the day-ahead market, suppliers specify quantities and minimum prices they are willing to accept and buyers pose bids with required quantities and maximum prices they are willing to pay. The price for each hour of the successive day is determined in an auction closing at 12AM by intersecting demand and supply curves, and taking into account the cross-border transmission constraint. As a result, the marginal price of electricity at which buyers and sellers are willing to exchange the quantity available becomes the electricity price paid by all. This pay as clear system implies that all the suppliers' offers are sorted by increasing price and those who are willing to accept less than the market price will sell their energy at the higher equilibrium market price, while the opposite happens with regards to buyers. This market system incentivizes suppliers to offer their product at their marginal cost of production, composed of the fuel cost, the start-up cost and the cost for emission allowances, given that receiving any price above this marginal cost would allow them to pay for their fixed costs as well. The second type of market countries engage in is the intraday market, where market participants trade continuously with delivery on the same day, in order to balance their electricity positions in response to oscillations in demand and production supply, closer to the time at which they are required. The fact that energy produced by renewables is sold at a lower marginal cost, given the absence of fuel and emission allowances cost, means that all renewable energy produced is exchanged before any other energy type. This is particularly useful given that renewable energy production is intermittent, characterized by large oscillations in power produced and is almost impossible to store. The size of the market demand, oscillating between 218 and 277 Giga Watt hour per month in 2019, however, makes it necessary that non renewable energy sources such as natural gas and coal are used to clear the market, meaning that electricity price is heavily dependent on the price of these prime commodities. This is demonstrated in the rising electricity prices today, due to the raise in natural gas prices.

Why is this happening

It is fair to say that the recent surge in natural gas prices is not the consequence of an individual “shock event” on the demand or supply side of the global natural gas market. In reality, there are multiple reasons for which Europe as well as many other parts of the globe are experiencing such fluctuations in the price of natural gas.

The Resurgence of Consumer Demand Post Covid

During the depths of the coronavirus pandemic, demand for goods and services fell as global savers managed to amass an additional $5.4tn (6% of Global GDP) according to figures published by credit rating agency Moody’s. Nevertheless, following the last two gruelling years of endless lockdowns, these consumer habits have been short lived. What must be said is that the global economic recovery has been much faster than expected as restrictions have been dropped in the vast majority of European nations (including the UK). For example, household marginal propensity to consume has risen at levels never seen before. This has been shown in Europe as GDP is expected to grow by 4.8% in euro-bearing countries over 2021 (according to the European Commission) and by 6.5% in the UK according to Rishi Sunday (The Chancellor of the Exchequer in the UK). These increases have correlated strongly with the increasing global gas demand of 3.6% (according to the IEA) as consumer spending for goods and services requiring natural gas (heating, refrigeration and hot water) has increased rapidly. As demand has increased, the price of natural gas has increased as shown below:

Figure 3: Natural Gas prices, year-to-date; $/per million British thermal units (MMBtu). Source: CNBC

The current increase in demand is now being amplified as the northern hemisphere slowly tends towards colder months where the demand for central heating (historically sourced by energy from burning coal and natural gas) historically increases.

Hence, as Europe has experienced rapid economic growth as it recovers from the international health crisis, demand within European markets has increased. As a result, demand for goods and services requiring natural gas has increased significantly leading to spiralling natural gas prices.

Climate Change pushing up the gas metre

As Europe was plunged into another lockdown in the bordering months of 2020 and 2021, European inventory levels of natural gas were particularly low heading into Autumn 2021 (storage sites in European countries and the UK are currently 72% full compared with 94% full at the same time a year ago according to Gas Infrastructure Europe data) . Due to particular cold weather and due to the fact that almost every being was at home for an extended period of time, natural gas supplies at the beginning of 2021 were wolfed down by increased consumer demand for heating and other services requiring natural gas. Additionally, levels of renewable energy were low in the first quarter of 2021 due to poor wind speeds and dry conditions. For example, German utility firm RWE reported “much lower” wind volumes in Northern and Central Europe for the first half of 2021 as wind speeds were below average, according to Reuters. In more simple terms, between October 2020 and March 2021, stores of alternative energy sources were truncated due to inadequate weather conditions which did not permit the production of renewable energy. Hence renewable energy supplies could not meet consumer demands.

All in all, the combination of these two independent factors limiting the supply of energy could only mean one thing - prices had to rise.

The Role of Russia

Although Europe imports much of its energy supplies from many different countries such as Iraq (9%), Nigeria and Saudi Arabia (both 8%) and Kazakhstan and Norway (both 7%), the vast majority of non-renewable energy imports are from Russia (27%). More specifically, 47% of EU natural gas imports are from the former Soviet state (according to www.statista.com). As a result, the EU has found itself particularly reliant on Russian supplies of natural gas. This has particularly impacted the EU’s incapability of importing natural gas as it has had to compete with other nations such as Belarus, Turkey and Kazakhstan who also depend on Russian gas supplies. This has thus meant that prices of natural gas produced by Gazprom (The superior natural gas supplier in Russia) have had to respond to increasing demand as gasless countries desperately compete for energy.

Moreover, due to political tensions in the Crimea region, Gazprom (the majority state-owned international energy firm in Russia) has on many occasions declined to ship additional supplies of gas via Ukraine to the EU as natural gas stores have dried up in continental Europe. Many surrounding countries have criticised Russia for “weaponizing” its supply of gas as they believe that it is being used as leverage as part of the controversial plan to build the Nord Stream 2 pipeline - a gas pipeline (which bypasses Ukraine) delivering energy supplies to Germany through the Baltic Sea. Hence, Russia’s reluctance to meet the EU’s demand for natural gas is likely to have led to an uptick in the market price for the energy source as supply has been actively restricted by the Russian Federal Assembly.

What’s the story like on the other side of the Pond?

The United States, unlike the EU, is much better equipped when it comes to energy crises like these.

Firstly, the US is the world’s largest producer of natural gas and currently, its inventory levels are not as dried up as those belonging to its European counterpart. Moreover, the US actually supplies itself with energy rather than importing all its energy from other nation-states. This can be shown by the fact that US natural gas imports are at their lowest levels in 26 years. This is thanks to many years of large-scale investment in mass-energy production. For example, right now, there are approximately 9,000 independent oil and natural gas producers in the United States according to the Independent Petroleum Association of America. Hence, gas prices have not been struck by potential shortages due to the existence of stable supply sources. What must also be mentioned is the fact that unlike the EU, the US is not having to compete desperately with other surrounding countries to gain access to natural gas supplies. Around the US lies many other major producers of natural gas such as Canada (5th largest producer in the world according to Wikipedia) as well as Trinidad and Tobago and Mexico. Population density in these countries is comparatively much lower than in the EU. This means that demand for natural gas is more stable, and hence the price is more stable.

Nevertheless, as one knows, due to climate change and global warming, it is not possible to conclude that the situation in the US will persist. One forgets that in February 2021, the state of Texas suffered a major power crisis due to severe winter storms which swept across the US over a two week period. As a result of this crisis, Texas natural gas production fell by 45% (according to www.utilitydive.com). As a result, despite normally costing $9.99 a month, the price of gas rose to $78 per hour as energy suppliers were having to raise prices given such drastic supply shortages.

Therefore, although it is clear that currently the US has not suffered like Europe has, one can’t predict the weather.

A novelty or nothing new?

The recent movement in gas prices may be the result of unprecedented events which mankind has never seen before its eyes. Nevertheless, if one steps back and looks through history, natural gas prices have on many occasions upticked to extortionate levels as seen in the following graph.

Hence, as Europe has experienced rapid economic growth as it recovers from the international health crisis, demand within European markets has increased. As a result, demand for goods and services requiring natural gas has increased significantly leading to spiralling natural gas prices.

Climate Change pushing up the gas metre

As Europe was plunged into another lockdown in the bordering months of 2020 and 2021, European inventory levels of natural gas were particularly low heading into Autumn 2021 (storage sites in European countries and the UK are currently 72% full compared with 94% full at the same time a year ago according to Gas Infrastructure Europe data) . Due to particular cold weather and due to the fact that almost every being was at home for an extended period of time, natural gas supplies at the beginning of 2021 were wolfed down by increased consumer demand for heating and other services requiring natural gas. Additionally, levels of renewable energy were low in the first quarter of 2021 due to poor wind speeds and dry conditions. For example, German utility firm RWE reported “much lower” wind volumes in Northern and Central Europe for the first half of 2021 as wind speeds were below average, according to Reuters. In more simple terms, between October 2020 and March 2021, stores of alternative energy sources were truncated due to inadequate weather conditions which did not permit the production of renewable energy. Hence renewable energy supplies could not meet consumer demands.

All in all, the combination of these two independent factors limiting the supply of energy could only mean one thing - prices had to rise.

The Role of Russia

Although Europe imports much of its energy supplies from many different countries such as Iraq (9%), Nigeria and Saudi Arabia (both 8%) and Kazakhstan and Norway (both 7%), the vast majority of non-renewable energy imports are from Russia (27%). More specifically, 47% of EU natural gas imports are from the former Soviet state (according to www.statista.com). As a result, the EU has found itself particularly reliant on Russian supplies of natural gas. This has particularly impacted the EU’s incapability of importing natural gas as it has had to compete with other nations such as Belarus, Turkey and Kazakhstan who also depend on Russian gas supplies. This has thus meant that prices of natural gas produced by Gazprom (The superior natural gas supplier in Russia) have had to respond to increasing demand as gasless countries desperately compete for energy.

Moreover, due to political tensions in the Crimea region, Gazprom (the majority state-owned international energy firm in Russia) has on many occasions declined to ship additional supplies of gas via Ukraine to the EU as natural gas stores have dried up in continental Europe. Many surrounding countries have criticised Russia for “weaponizing” its supply of gas as they believe that it is being used as leverage as part of the controversial plan to build the Nord Stream 2 pipeline - a gas pipeline (which bypasses Ukraine) delivering energy supplies to Germany through the Baltic Sea. Hence, Russia’s reluctance to meet the EU’s demand for natural gas is likely to have led to an uptick in the market price for the energy source as supply has been actively restricted by the Russian Federal Assembly.

What’s the story like on the other side of the Pond?

The United States, unlike the EU, is much better equipped when it comes to energy crises like these.

Firstly, the US is the world’s largest producer of natural gas and currently, its inventory levels are not as dried up as those belonging to its European counterpart. Moreover, the US actually supplies itself with energy rather than importing all its energy from other nation-states. This can be shown by the fact that US natural gas imports are at their lowest levels in 26 years. This is thanks to many years of large-scale investment in mass-energy production. For example, right now, there are approximately 9,000 independent oil and natural gas producers in the United States according to the Independent Petroleum Association of America. Hence, gas prices have not been struck by potential shortages due to the existence of stable supply sources. What must also be mentioned is the fact that unlike the EU, the US is not having to compete desperately with other surrounding countries to gain access to natural gas supplies. Around the US lies many other major producers of natural gas such as Canada (5th largest producer in the world according to Wikipedia) as well as Trinidad and Tobago and Mexico. Population density in these countries is comparatively much lower than in the EU. This means that demand for natural gas is more stable, and hence the price is more stable.

Nevertheless, as one knows, due to climate change and global warming, it is not possible to conclude that the situation in the US will persist. One forgets that in February 2021, the state of Texas suffered a major power crisis due to severe winter storms which swept across the US over a two week period. As a result of this crisis, Texas natural gas production fell by 45% (according to www.utilitydive.com). As a result, despite normally costing $9.99 a month, the price of gas rose to $78 per hour as energy suppliers were having to raise prices given such drastic supply shortages.

Therefore, although it is clear that currently the US has not suffered like Europe has, one can’t predict the weather.

A novelty or nothing new?

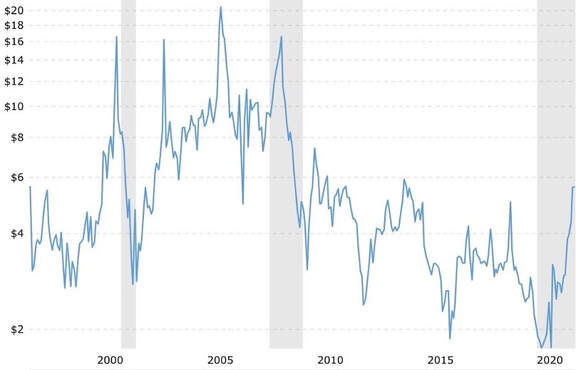

The recent movement in gas prices may be the result of unprecedented events which mankind has never seen before its eyes. Nevertheless, if one steps back and looks through history, natural gas prices have on many occasions upticked to extortionate levels as seen in the following graph.

Figure 4: Historical natural gas price levels. Source: Macrotrends

Over the Global Financial Crisis of 2008, natural gas prices exceeded $16 per million BTU (British Thermal Unit - the amount of heat required to raise the temperature of one pound of water by one degree Fahrenheit). This was due to extreme weather events such hurricanes Gustav and Ike which caused multiple production shut-ins in the Gulf of Mexico and Louisiana. In summer 2000, gas prices peaked at a similar price as according to industry experts, the use of natural gas for electric generation increased at a significant rate hence increasing demand for natural gas causing demand-pull inflation.

In fairness, the recent spikes in gas prices have not yet matched those in ‘08 and ‘00 ($16.5 per million BTU in both years respectively). Nevertheless, with rising fears of winter lockdowns and extreme cold weather, it is undeniable that gas prices could reach new heights in the near future.

Natural Gas: A bridge to the future?

Natural gas is a gas mixture composed mainly of methane (usually more than 85%) and other hydrocarbons such as ethane and propane. It is burned to provide heat for cooking and heating, to fuel thermoelectric power stations and is frequently used as raw material, for example in the production of plastics and paints. Natural gas characteristics make it increasingly important compared to other fossil fuels, given the role it is allocated in the transition to cleaner energy sources. Methane, the main component of natural gas, has the lowest carbon to hydrogen ratio among hydrocarbons, meaning that it produces less carbon dioxide when combusted compared to other fuels such as coal and oil. Furthermore, power plants producing electricity through natural gas are more flexible since they can be more easily and conveniently activated when in need of energy. This property makes it especially efficient in combination with renewable energies, given that their inconstant energy production needs to be covered with alternative energy production methods when they become unable to clear out market demand. In addition to these advantages in terms of cleaner electricity production, the possibility to transport natural gas in liquid state called LNG (Liquid Natural Gas) makes it versatile as a low emission transport fuel and useful while trying to respond to short term disruptions, since it can be easily shipped or transported through underground pipelines. The multiple benefits brought from the use of this fuel are the reason why it’s exclusion from the European Taxonomy of green activities has been debated and criticized. Given that the cost of decarbonising the energy sector is estimated to be equal to 350 billion between public and private investment, natural gas would provide the opportunity to spread these costs over a longer time frame, by gradually shifting to cleaner energy sources. This dilution of investments could aid especially countries in Eastern Europe such as Poland, Czechia, Romania and Bulgaria, which have the highest dependence on coal for energy production. Transitioning to natural gas would allow them to start reducing emissions, while starting to invest on renewable energies, making them more capable of reaching the 55% emission reduction target set by the EU for 2030. The exclusion of natural gas from the taxonomy is likely to divert investments from this sector and widen the gap of environmental transition progress between these Eastern Europe countries and the rest of Europe.

In addition to being used as a fuel in itself, natural gas is gaining importance also thanks to its use in hydrogen production. Hydrogen is a fuel which burns with oxygen to produce energy and water, contrarily to fossil fuels which also emit carbon dioxide and harmful gases. The reason why hydrogen is preferred to other clean energy forms is that it can be stored in liquid form, such that it can be used as a fuel for transportation or to provide residential heating without revolutionizing the transmission systems currently used. In fact, liquid hydrogen can be blended with natural gas and can be safely transported within the existing natural gas pipelines. This characteristic allows a faster and less expensive decrease in carbon emissions in the energy sector compared to the revolution that would be required with renewable energies. The controversy with respect to the use of hydrogen stands on the fact that currently 48% of it is produced with natural gas, 30% with oil and 18% with coal, all non renewable and polluting energy sources. To prevent the pollution generated by producing hydrogen this way, Carbon Capture, Utilization and Storage technologies (CCUS) are being developed to collect CO2 and to ensure it can be used in other processes such as the production of ammonia or as a refrigerant in nuclear stations. In this way, natural gas can be used to produce hydrogen, while ensuring that the carbon dioxide produced is not released into the atmosphere.

Future repercussions

Finally, it is important to analyse the possible consequences of this situation.

Short term effect of the rise of natural gas and coal is higher electricity prices and then higher household energy bills. For this reason, many governments have taken measures to alleviate electricity bills, to release the pressure on consumers. Current market dynamics (forward curves as of the beginning of October) suggest that European benchmarks for natural gas (TTF) and coal (Rotterdam coal) will remain high compared to last year and according to the World Bank’s forecast they will start to decrease in the second half of 2022 as supply constraints ease. Prices of both natural gas and electricity will fluctuate in Europe depending on temperatures, wind output and other factors such as green revolution, political patterns. Regarding Covid 19, vaccinations will probably break the link between the pandemic, transport and natural gas prices.

Medium-long term effects may be a slowdown of the transition to a cleaner world, indeed, according to EU taxonomy, natural gas is not included into transitional activities even if it provides a viable alternative to fuel for transport, reducing emissions from maritime and heavy road transport. The fact that their prices will remain high further disincentives the use of natural gas as a substitute to fuel.

To fight these controversies, most members of the European commission claimed actions at national level and, even if EC cannot directly avoid gas price movements, It has investigated possible “manipulative practices or abuse” by companies producing natural gas. The only thing that EC can manipulate is taxes, with the aim of helping the most vulnerable consumers.

One important step made by the EU commission is the comprehensive legislative package named “Fit for 55” designed to revise the EU 2030 climate and energy framework. In particolar one important aspect is the decarbonization of gas market and the establishment of hydrogen market.

In conclusion, considering forecasts of major investment banks such as JPM and Citi, Industrial commodities are expected to remain well-supported, due to green and digital revolutions, brent Oil will decrease in 2022/2023 and also natural gas tension is expected to dissipate in 2022. The most controversial commodity is copper, that will become more and more important because it is fundamental for building electric items (in particular cars) and components of technological devices such as computers. All these aspects will probably influence its price.

Sources

Chiara Cerrato, Sofia Frasson, Boaz Lister

In fairness, the recent spikes in gas prices have not yet matched those in ‘08 and ‘00 ($16.5 per million BTU in both years respectively). Nevertheless, with rising fears of winter lockdowns and extreme cold weather, it is undeniable that gas prices could reach new heights in the near future.

Natural Gas: A bridge to the future?

Natural gas is a gas mixture composed mainly of methane (usually more than 85%) and other hydrocarbons such as ethane and propane. It is burned to provide heat for cooking and heating, to fuel thermoelectric power stations and is frequently used as raw material, for example in the production of plastics and paints. Natural gas characteristics make it increasingly important compared to other fossil fuels, given the role it is allocated in the transition to cleaner energy sources. Methane, the main component of natural gas, has the lowest carbon to hydrogen ratio among hydrocarbons, meaning that it produces less carbon dioxide when combusted compared to other fuels such as coal and oil. Furthermore, power plants producing electricity through natural gas are more flexible since they can be more easily and conveniently activated when in need of energy. This property makes it especially efficient in combination with renewable energies, given that their inconstant energy production needs to be covered with alternative energy production methods when they become unable to clear out market demand. In addition to these advantages in terms of cleaner electricity production, the possibility to transport natural gas in liquid state called LNG (Liquid Natural Gas) makes it versatile as a low emission transport fuel and useful while trying to respond to short term disruptions, since it can be easily shipped or transported through underground pipelines. The multiple benefits brought from the use of this fuel are the reason why it’s exclusion from the European Taxonomy of green activities has been debated and criticized. Given that the cost of decarbonising the energy sector is estimated to be equal to 350 billion between public and private investment, natural gas would provide the opportunity to spread these costs over a longer time frame, by gradually shifting to cleaner energy sources. This dilution of investments could aid especially countries in Eastern Europe such as Poland, Czechia, Romania and Bulgaria, which have the highest dependence on coal for energy production. Transitioning to natural gas would allow them to start reducing emissions, while starting to invest on renewable energies, making them more capable of reaching the 55% emission reduction target set by the EU for 2030. The exclusion of natural gas from the taxonomy is likely to divert investments from this sector and widen the gap of environmental transition progress between these Eastern Europe countries and the rest of Europe.

In addition to being used as a fuel in itself, natural gas is gaining importance also thanks to its use in hydrogen production. Hydrogen is a fuel which burns with oxygen to produce energy and water, contrarily to fossil fuels which also emit carbon dioxide and harmful gases. The reason why hydrogen is preferred to other clean energy forms is that it can be stored in liquid form, such that it can be used as a fuel for transportation or to provide residential heating without revolutionizing the transmission systems currently used. In fact, liquid hydrogen can be blended with natural gas and can be safely transported within the existing natural gas pipelines. This characteristic allows a faster and less expensive decrease in carbon emissions in the energy sector compared to the revolution that would be required with renewable energies. The controversy with respect to the use of hydrogen stands on the fact that currently 48% of it is produced with natural gas, 30% with oil and 18% with coal, all non renewable and polluting energy sources. To prevent the pollution generated by producing hydrogen this way, Carbon Capture, Utilization and Storage technologies (CCUS) are being developed to collect CO2 and to ensure it can be used in other processes such as the production of ammonia or as a refrigerant in nuclear stations. In this way, natural gas can be used to produce hydrogen, while ensuring that the carbon dioxide produced is not released into the atmosphere.

Future repercussions

Finally, it is important to analyse the possible consequences of this situation.

Short term effect of the rise of natural gas and coal is higher electricity prices and then higher household energy bills. For this reason, many governments have taken measures to alleviate electricity bills, to release the pressure on consumers. Current market dynamics (forward curves as of the beginning of October) suggest that European benchmarks for natural gas (TTF) and coal (Rotterdam coal) will remain high compared to last year and according to the World Bank’s forecast they will start to decrease in the second half of 2022 as supply constraints ease. Prices of both natural gas and electricity will fluctuate in Europe depending on temperatures, wind output and other factors such as green revolution, political patterns. Regarding Covid 19, vaccinations will probably break the link between the pandemic, transport and natural gas prices.

Medium-long term effects may be a slowdown of the transition to a cleaner world, indeed, according to EU taxonomy, natural gas is not included into transitional activities even if it provides a viable alternative to fuel for transport, reducing emissions from maritime and heavy road transport. The fact that their prices will remain high further disincentives the use of natural gas as a substitute to fuel.

To fight these controversies, most members of the European commission claimed actions at national level and, even if EC cannot directly avoid gas price movements, It has investigated possible “manipulative practices or abuse” by companies producing natural gas. The only thing that EC can manipulate is taxes, with the aim of helping the most vulnerable consumers.

One important step made by the EU commission is the comprehensive legislative package named “Fit for 55” designed to revise the EU 2030 climate and energy framework. In particolar one important aspect is the decarbonization of gas market and the establishment of hydrogen market.

In conclusion, considering forecasts of major investment banks such as JPM and Citi, Industrial commodities are expected to remain well-supported, due to green and digital revolutions, brent Oil will decrease in 2022/2023 and also natural gas tension is expected to dissipate in 2022. The most controversial commodity is copper, that will become more and more important because it is fundamental for building electric items (in particular cars) and components of technological devices such as computers. All these aspects will probably influence its price.

Sources

- European Power Exchange Spot

- Gestore Mercati Elettrici

- Shell.com

- Enbridgegas.com

- US Energy Information Administration

- Eurostat

- Financial Times

- CNBC

- International Energy Agency

- European Commission

- Reuters

- Wikipedia

- Statista.com

- Petroleum Association of America

- Utilitydive.com

- Macrotrends.net

- Forbes

- WorldBank.org

- Yahoo Finance

- Citibank/Insights

- JPM/Insights

- IEA

Chiara Cerrato, Sofia Frasson, Boaz Lister