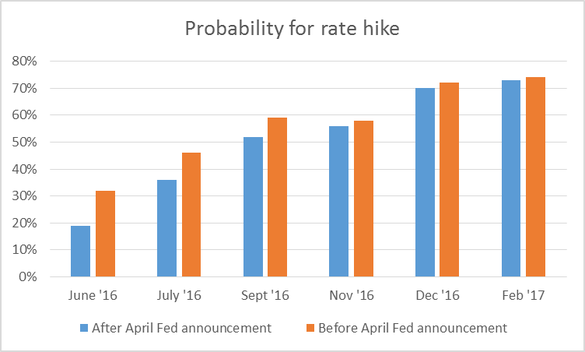

As a ship sailing in the storm waiting for captain’s directions, global markets last week have been reacting wildly to several controversial news making Janet Yellen and all her colleagues of main worldwide central banks spend sleepless nights.

Looking at the current situation from an overall perspective, it cannot be denied that everybody is waiting for the Fed to provide guidance about the economy through the decision concerning American monetary policy scheduled next month. Somebody could argue that the burden should not be placed completely over Ms. Yellen’s shoulders. However, empirical evidence on Forex markets backs the idea that Mario Draghi (ECB president), not to mention Haruhiko Kuroda (Bank of Japan president), have nowadays relatively low impact with respect to Fed Chairman’s words.

The aim of this article is trying to disentangle the overall effects on capital markets caused by all the recent news in order to answer the question: will Janet Yellen confirm next month her decision of restrictive monetary policy in the US or not?

Looking at the current situation from an overall perspective, it cannot be denied that everybody is waiting for the Fed to provide guidance about the economy through the decision concerning American monetary policy scheduled next month. Somebody could argue that the burden should not be placed completely over Ms. Yellen’s shoulders. However, empirical evidence on Forex markets backs the idea that Mario Draghi (ECB president), not to mention Haruhiko Kuroda (Bank of Japan president), have nowadays relatively low impact with respect to Fed Chairman’s words.

The aim of this article is trying to disentangle the overall effects on capital markets caused by all the recent news in order to answer the question: will Janet Yellen confirm next month her decision of restrictive monetary policy in the US or not?

|

Yes

|

No

|

Currency: the dollar hit an 18-month low against the yen of ¥105.52 on Tuesday. Similarly, the euro broke back above $1.15 for the first time since August. This shows how, no matter Draghi’s stimulus, only Yellen’s decision will determine exchange rate direction.

Gold and Oil: gold tracked dollar moves surpassing 1300$ an ounce for the first time since January 2015. Oil had a volatile session as market participants continued to weigh up the potential impact on supply of the devastating wildfire in Canada’s oil sands region.

Laporta Davide