Argentina is suffering a period of hyperinflation and hyper-devaluation of its currency, the Peso.

However, the Argentine government has in mind an interesting and peculiar method to solve the situation : “The Malbec Dollar”.

However, the Argentine government has in mind an interesting and peculiar method to solve the situation : “The Malbec Dollar”.

Overview

In George Orwell’s “Animal Farm”, the pigs mischievously stated: “All animals are equal, but some animals are more equal than others”, and this certainly seems to be the case regarding dollar bills in Argentina, a country suffering from severe hyper-inflation, austerity measures and very low currency reserves. Argentinians’ love for US dollars, or rather fear of their own Argentine peso, is so evident that trading a $100-dollar bill will get you more pesos (if you are willing to trade it) than two $50-dollar bills, or any other bundle adding up to 100 for that matter.

However, owning dollars is not a new trend, and Argentines have used dollars to hedge against declining purchasing power for many years, so much so that in 2020 the central bank estimated that the people hold $170bn in cash in the country, or about a fifth of all dollars in circulation outside the US at that time.

In George Orwell’s “Animal Farm”, the pigs mischievously stated: “All animals are equal, but some animals are more equal than others”, and this certainly seems to be the case regarding dollar bills in Argentina, a country suffering from severe hyper-inflation, austerity measures and very low currency reserves. Argentinians’ love for US dollars, or rather fear of their own Argentine peso, is so evident that trading a $100-dollar bill will get you more pesos (if you are willing to trade it) than two $50-dollar bills, or any other bundle adding up to 100 for that matter.

However, owning dollars is not a new trend, and Argentines have used dollars to hedge against declining purchasing power for many years, so much so that in 2020 the central bank estimated that the people hold $170bn in cash in the country, or about a fifth of all dollars in circulation outside the US at that time.

Argentina’s inflation rate far outpaced that of its main trade partners and gave the country the much unwanted crown for worst performing economy in the G20.

Source: Financial Times

Source: Financial Times

These billions of dollars that people own, however, stand in stark contrast with the low net currency reserves (gross reserves less foreign short- term borrowing and foreign deposits in the Central Bank) the country has: around $4.4bn for a country of around 45m inhabitants.

Under Argentina's $44 billion credit 30-months agreement with the International Monetary Fund (IMF), the country has committed to increasing its international reserves and reducing its fiscal deficit. To achieve this, the government has pledged to decrease its fiscal deficit from 3 per cent of gross domestic product in 2021 to 2.5 per cent in 2022, 1.9 per cent this year, and 0.9 per cent in 2024.

Furthermore, the government has introduced multiple favourable exchange rates (such as one for tourists, one for Argentines travelling to Qatar to see their team play – and win- the World Cup and one for soy exporters) to incentivize people to trade their dollars for pesos.

The Malbec Dollar

The latest Argentine experiment in this long list of rates is the Malbec Dollar, which aims to provide an advantageous exchange rate for exporters of the famous Argentinian wine. Although still among the largest exporters of wine, Argentina’s production has dropped significantly from the all-time high hit 2021, due to a series of factors including droughts, late frosts and high inflation, which cut into vineyards’ profits.

The Malbec dollar aims to ease the pressure put on the system, by allowing producers to exchange dollars at a premium, and, while we must wait until April to find out the exact numbers, it is a clear incentive to boost exports and replenish the foreign currency reserves. This exchange rate policy is one of the measures the government is taking to fulfill its commitment to the IMF. This rate would be probably followed by further preferential rates for other local products such as lemons and cotton.

Argentina's Finance Minister, Sergio Massa, announced this month that the preferential exchange rate for wine is intended to "help recover export competitiveness and help consolidate Argentina's reserves." The exchange rate policy aims to ensure that the price of wine does not soar domestically and to provide support to vineyards that are struggling due to the high inflation rate and poor harvests.

Indeed, Argentina is one of the world's top 10 wine exporters in dollar terms. However, the country experienced a 20 per cent drop in bulk wine exports by value in 2022, and overall wine production fell by a fifth compared to the previous year. The 2023 harvest, which will end in late April, is expected to be one of the worst in a decade, according to experts.

However, the government may find it difficult to replicate the success of the soy dollar policy in the wine sector due to the longer production times for wine. Critics of the government's preferential exchange rate policies argue that those measures are a way to avoid devaluing the currency. In the past three years, the government has introduced at least ten different preferential exchange rates for various sectors. Buenos Aires-based economist Fernando Marengo believes that the ruling Peronist government "does not want to take on the cost of devaluing in an election year" because it could lead to higher inflation, rising poverty, and social unrest. Moreover, general elections are scheduled to take place in October.

The Blue market

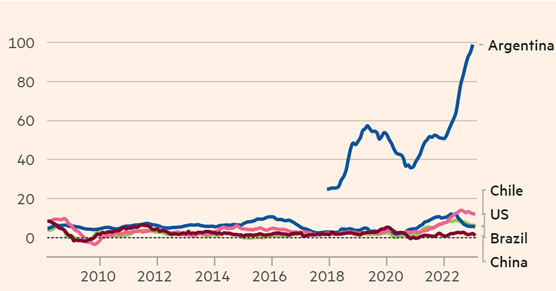

Even though the Malbec dollar will incentive exports, and aid in enlarging the current account surplus, it still fails to address the prominent problem of the nation’s currency: overvaluation. As mentioned before, these preferential exchange rates can be viewed as a short-term solution for the government plan to increase currency reserves and stall the devaluation of the peso. There are plenty of arguments that indicate that the peso should fall as much as 30% to be in sync with the fundamentals, but perhaps the most conclusive measures are seen within the Blue Market and the REER (real effective exchange rate).

The Blue Market represents the black-market exchanges on the streets that provide a much better rate than banks, while REER measures the currency in relation to a weighted average of an index or basket of major currencies, divided by the price deflator or index costs. The “dollar blue” trades at 50% less than the official rate, while the REER is assuming alarmingly high values, despite the strengthening of the other currencies of the other countries in the reference basket.

Under Argentina's $44 billion credit 30-months agreement with the International Monetary Fund (IMF), the country has committed to increasing its international reserves and reducing its fiscal deficit. To achieve this, the government has pledged to decrease its fiscal deficit from 3 per cent of gross domestic product in 2021 to 2.5 per cent in 2022, 1.9 per cent this year, and 0.9 per cent in 2024.

Furthermore, the government has introduced multiple favourable exchange rates (such as one for tourists, one for Argentines travelling to Qatar to see their team play – and win- the World Cup and one for soy exporters) to incentivize people to trade their dollars for pesos.

The Malbec Dollar

The latest Argentine experiment in this long list of rates is the Malbec Dollar, which aims to provide an advantageous exchange rate for exporters of the famous Argentinian wine. Although still among the largest exporters of wine, Argentina’s production has dropped significantly from the all-time high hit 2021, due to a series of factors including droughts, late frosts and high inflation, which cut into vineyards’ profits.

The Malbec dollar aims to ease the pressure put on the system, by allowing producers to exchange dollars at a premium, and, while we must wait until April to find out the exact numbers, it is a clear incentive to boost exports and replenish the foreign currency reserves. This exchange rate policy is one of the measures the government is taking to fulfill its commitment to the IMF. This rate would be probably followed by further preferential rates for other local products such as lemons and cotton.

Argentina's Finance Minister, Sergio Massa, announced this month that the preferential exchange rate for wine is intended to "help recover export competitiveness and help consolidate Argentina's reserves." The exchange rate policy aims to ensure that the price of wine does not soar domestically and to provide support to vineyards that are struggling due to the high inflation rate and poor harvests.

Indeed, Argentina is one of the world's top 10 wine exporters in dollar terms. However, the country experienced a 20 per cent drop in bulk wine exports by value in 2022, and overall wine production fell by a fifth compared to the previous year. The 2023 harvest, which will end in late April, is expected to be one of the worst in a decade, according to experts.

However, the government may find it difficult to replicate the success of the soy dollar policy in the wine sector due to the longer production times for wine. Critics of the government's preferential exchange rate policies argue that those measures are a way to avoid devaluing the currency. In the past three years, the government has introduced at least ten different preferential exchange rates for various sectors. Buenos Aires-based economist Fernando Marengo believes that the ruling Peronist government "does not want to take on the cost of devaluing in an election year" because it could lead to higher inflation, rising poverty, and social unrest. Moreover, general elections are scheduled to take place in October.

The Blue market

Even though the Malbec dollar will incentive exports, and aid in enlarging the current account surplus, it still fails to address the prominent problem of the nation’s currency: overvaluation. As mentioned before, these preferential exchange rates can be viewed as a short-term solution for the government plan to increase currency reserves and stall the devaluation of the peso. There are plenty of arguments that indicate that the peso should fall as much as 30% to be in sync with the fundamentals, but perhaps the most conclusive measures are seen within the Blue Market and the REER (real effective exchange rate).

The Blue Market represents the black-market exchanges on the streets that provide a much better rate than banks, while REER measures the currency in relation to a weighted average of an index or basket of major currencies, divided by the price deflator or index costs. The “dollar blue” trades at 50% less than the official rate, while the REER is assuming alarmingly high values, despite the strengthening of the other currencies of the other countries in the reference basket.

Real Effective Exchange Rate (CPI = 100, Jan 2001)

Source: Sperrfechter, K. (2023) “Malbec dollar” won’t save Argentina from devaluation, Capital Economics. (Accessed: March 23, 2023)

Source: Sperrfechter, K. (2023) “Malbec dollar” won’t save Argentina from devaluation, Capital Economics. (Accessed: March 23, 2023)

Stalling to align the currency with its true value can prove to be detrimental for the country, but its devaluing is out of discussion for the near future, as elections near. Thus, policies like the “Malbec dollar” or the “Soy dollar”, along with strict capital controls, seem to be the only tools available to the current government to bolster the economy and reintegrate the country in international capital markets. If these fail to achieve their goal, the devaluation could cause inflation to ramp up even further, making imports more costly, and thus rendering the IMF deal obsolete.

Three-digit inflation and its extreme adverse effects

The economy worldwide has been plagued by high inflation rates, and the consequences have been catastrophic. From the pension fund crisis in England at the end of last year, to the bank runs we see today, inflation and the way Central Banks and consumers dealt with it left severe scars in economies worldwide. While these events happened in countries where inflation is still in the single digits, Argentina has been plagued by rates as high as 100%

This implies some extreme adverse side-effects that severely affect consumer spending decisions and market dynamics. For example, Argentinians spend their entire paycheck as soon as they receive it, stockpiling food, and household items, knowing that by next month prices will have significantly risen, while their wages are lagging behind.

Consumers that can’t afford even the necessities resort to payment plans that span over extremely long periods. Since inflation outpaces the highest of interest rates, deferred payments allow the people to make the most out of their money. Another way citizens are saving is by paying their taxes months after they are due, so they depreciate. This in turn creates serious cashflow problems for the Government that simply resorts to “printing” more money thus blowing tailwinds into the inflationary cycles.

Previous exchange rate schemes in Argentina

The idea of fostering production and exports in certain sectors by instituting special exchange rates is not unique to the case of the ‘Malbec dollar’. Argentina has in fact introduced a similar system on its soy industry in September of 2022, to prop up exports of the crop and its derivatives and to secure an inflow of US dollars into its dwindling foreign currency reserves.

The program at its start allowed an exchange rate of around 200 pesos on the dollar compared to the official rate of 150. In late November it was reintroduced with an even higher exchange rate of 230 pesos on the dollar.

The initial program in September brought around USD 5 billion dollars of reserves to the central bank. The reintroduction of the program has not fared so successfully as many farmers choose to stock up on produce instead of selling as the peso is rapidly falling in value, and others had no stock left as they had already sold it during the first month of the program.

The economy worldwide has been plagued by high inflation rates, and the consequences have been catastrophic. From the pension fund crisis in England at the end of last year, to the bank runs we see today, inflation and the way Central Banks and consumers dealt with it left severe scars in economies worldwide. While these events happened in countries where inflation is still in the single digits, Argentina has been plagued by rates as high as 100%

This implies some extreme adverse side-effects that severely affect consumer spending decisions and market dynamics. For example, Argentinians spend their entire paycheck as soon as they receive it, stockpiling food, and household items, knowing that by next month prices will have significantly risen, while their wages are lagging behind.

Consumers that can’t afford even the necessities resort to payment plans that span over extremely long periods. Since inflation outpaces the highest of interest rates, deferred payments allow the people to make the most out of their money. Another way citizens are saving is by paying their taxes months after they are due, so they depreciate. This in turn creates serious cashflow problems for the Government that simply resorts to “printing” more money thus blowing tailwinds into the inflationary cycles.

Previous exchange rate schemes in Argentina

The idea of fostering production and exports in certain sectors by instituting special exchange rates is not unique to the case of the ‘Malbec dollar’. Argentina has in fact introduced a similar system on its soy industry in September of 2022, to prop up exports of the crop and its derivatives and to secure an inflow of US dollars into its dwindling foreign currency reserves.

The program at its start allowed an exchange rate of around 200 pesos on the dollar compared to the official rate of 150. In late November it was reintroduced with an even higher exchange rate of 230 pesos on the dollar.

The initial program in September brought around USD 5 billion dollars of reserves to the central bank. The reintroduction of the program has not fared so successfully as many farmers choose to stock up on produce instead of selling as the peso is rapidly falling in value, and others had no stock left as they had already sold it during the first month of the program.

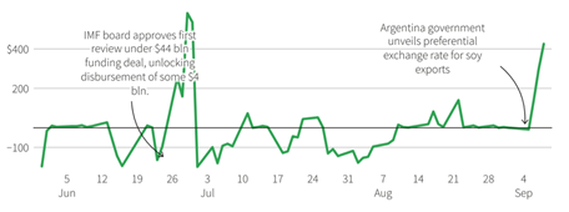

Daily Argentina central bank purchases or sales of dollars in millions of USD

Source: BCRA, traders

Source: BCRA, traders

One of the main reasons for the original program’s success was the substantial Chinese interest for the country’s soy produce: In September, China bought 3.8 million tons of soy as a part of the program on top of its existing imports from Argentina, largely exhausting the latter’s existing stockpiles.

Supply towards exports though is not only limited by available stock, but also by the fierce competition of domestic soy crushing companies, which have started to bid higher prices for the plant after the government liberalized the market of biodiesel.

Because of these factors, Argentinian soybeans have become less competitive in the global market. For example, both US and Brazilian produced soy are cheaper now, while Argentina is lagging behind its competition.

Although the ‘Malbec dollar’ scheme also faces its fair share of challenges, wine is a much less commodified product than soybeans, so a similar scenario to the soybean program is unlikely to play out as customers tend to be less price sensitive in the wine market.

Supply towards exports though is not only limited by available stock, but also by the fierce competition of domestic soy crushing companies, which have started to bid higher prices for the plant after the government liberalized the market of biodiesel.

Because of these factors, Argentinian soybeans have become less competitive in the global market. For example, both US and Brazilian produced soy are cheaper now, while Argentina is lagging behind its competition.

Although the ‘Malbec dollar’ scheme also faces its fair share of challenges, wine is a much less commodified product than soybeans, so a similar scenario to the soybean program is unlikely to play out as customers tend to be less price sensitive in the wine market.

Conclusion

While it is still early to predict how these measures will pan out, there is hope for the South American country: having sealed a new deal with the IMF in 2022 and with previous preferential exchange rates showing great potential, the government in Buenos Aires finally seems to have a plan to tackle inflation, which is forecasted to peak this year. Diplomatic efforts have also gone a long way in earning the trust of trading partners, such as Brazil, with the governments of the two countries announcing they plan on creating a common currency and with general elections later this year, 2023 looks to be a make-or-break year for La Albiceleste. One thing is certain, however: even if the country will succeed in tackling all their economic problems, it will not happen overnight. And until they can win back the trust of foreign investors, the Argentinian people will continue to struggle.

While it is still early to predict how these measures will pan out, there is hope for the South American country: having sealed a new deal with the IMF in 2022 and with previous preferential exchange rates showing great potential, the government in Buenos Aires finally seems to have a plan to tackle inflation, which is forecasted to peak this year. Diplomatic efforts have also gone a long way in earning the trust of trading partners, such as Brazil, with the governments of the two countries announcing they plan on creating a common currency and with general elections later this year, 2023 looks to be a make-or-break year for La Albiceleste. One thing is certain, however: even if the country will succeed in tackling all their economic problems, it will not happen overnight. And until they can win back the trust of foreign investors, the Argentinian people will continue to struggle.

By Dinu Cionga, Vittoria Palmieri, Matei Sandru, Mate Mangoff.

Bibliography

Argus Media

BCRA (Banco Central de la República Argentina)

Buenos Aires Times

Capital Economics

Capital Economics

Financial Times

International Monetary Fund

Reuters

Trading economics

Wall Street Journal

Argus Media

BCRA (Banco Central de la República Argentina)

Buenos Aires Times

Capital Economics

Capital Economics

Financial Times

International Monetary Fund

Reuters

Trading economics

Wall Street Journal