The US economy is hitting maximum levels of employment and inflation, and, in response, Janet Yellen, Chair of the Federal Reserve, is expected to accelerate the pace of interest rate increases.

More than two weeks ago derivatives markets were pricing in a 98% probability that the Fed would raise interest rates by 0.25 % in its last meeting on the back of strong US employment data releases.

Although the US central bank eventually decided not to raise interest rates, ahead of the last meeting this month investors had placed significant bets on a fall in bond prices via three ETFs, all run by Blackrock. The rise in ETF short positions has coincided with the largest weekly redemptions from actively managed high-yield corporate bond funds since the US election in November.

Although this is how most of the market players had reacted to the expected increase in interest rates in the last Fed meeting, betting against these large bond funds with different maturities is definitely not the strategy that many institutional investors should, or /can, consider. In fact, most of the pension funds and insurance companies have to follow LDI strategies, which often imply large long-only positions in government bonds.

However, also these market players can find some strategies which are able to maximize their expected payoff with rising interest rates.

In the current market environment longer maturities should be preferred to shorter ones by institutional investors. Passive strategies such as the barbell or the bond ladders may play a crucial role in the portfolio of many pension funds, insurance companies as well as other bond funds.

In order to understand why these investors should prefer longer maturities, let’s consider the nature of the “term premium” paid by long-term Treasuries.

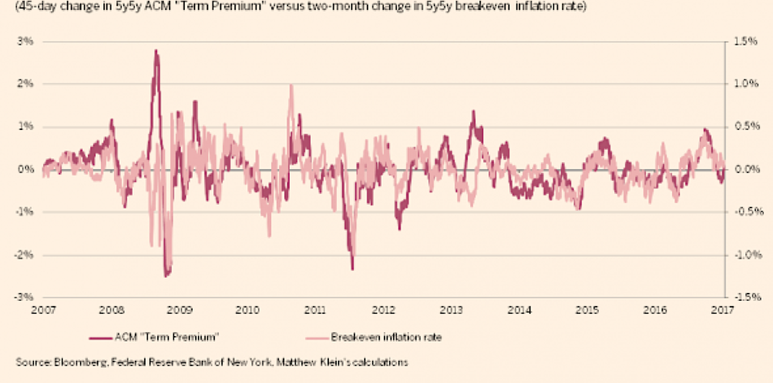

Surprisingly, if we look at the historical changes in both term premium and inflation breakeven rates, we can observe a high correlation between the two, with the change in the inflation breakeven rate generally half as big as the corresponding change in the term premium. The chart below displays this relation using 45-day change in 5y5y ACM term premium versus 2-month change in 5y5y breakeven inflation rate.

More than two weeks ago derivatives markets were pricing in a 98% probability that the Fed would raise interest rates by 0.25 % in its last meeting on the back of strong US employment data releases.

Although the US central bank eventually decided not to raise interest rates, ahead of the last meeting this month investors had placed significant bets on a fall in bond prices via three ETFs, all run by Blackrock. The rise in ETF short positions has coincided with the largest weekly redemptions from actively managed high-yield corporate bond funds since the US election in November.

Although this is how most of the market players had reacted to the expected increase in interest rates in the last Fed meeting, betting against these large bond funds with different maturities is definitely not the strategy that many institutional investors should, or /can, consider. In fact, most of the pension funds and insurance companies have to follow LDI strategies, which often imply large long-only positions in government bonds.

However, also these market players can find some strategies which are able to maximize their expected payoff with rising interest rates.

In the current market environment longer maturities should be preferred to shorter ones by institutional investors. Passive strategies such as the barbell or the bond ladders may play a crucial role in the portfolio of many pension funds, insurance companies as well as other bond funds.

In order to understand why these investors should prefer longer maturities, let’s consider the nature of the “term premium” paid by long-term Treasuries.

Surprisingly, if we look at the historical changes in both term premium and inflation breakeven rates, we can observe a high correlation between the two, with the change in the inflation breakeven rate generally half as big as the corresponding change in the term premium. The chart below displays this relation using 45-day change in 5y5y ACM term premium versus 2-month change in 5y5y breakeven inflation rate.

Normally, the breakeven inflation rate should correspond to the expected inflation rate plus the inflation risk premium minus the TIPS liquidity premium. Therefore, it should not be affected by the risk premium compensating investors for uncertainty about long-term real interest rates.

This prompts us to ask ourselves why the breakeven inflation rate is so tightly correlated to the term premium.

Given that the Fed sets its target for the US inflation rate slightly below 2% and the market expects the US central bank to act consistently with its (double) mandate, we can reasonably assume that, at the moment, long-term inflation expectations implied by the market willdo not move – this is indeed the same position as the one of the NY Fed economists.

Secondly, we can also reasonably assume that changes in the TIPS liquidity premium are generally small, as typically happens in normal market conditions.

Therefore, by following this reasoning, changes in breakeven inflation rates are mainly due to changes in the inflation risk premium. The consequence of this is that the term premium is mainly linked to changes in the uncertainty about inflation forecasts, even though it remains challenging to disentangle actual changes in expectations about inflation and real rates from changes in the uncertainty about these expectations.

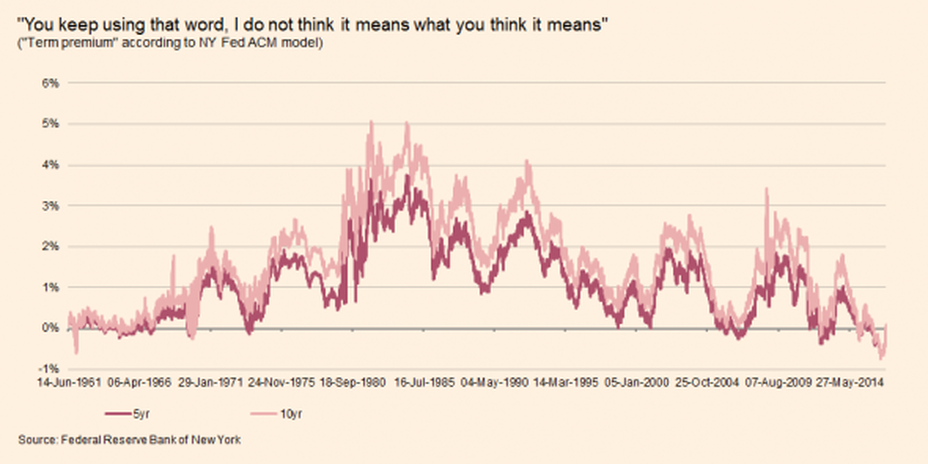

On a different note, it also interesting to look at the difference between the implied 5-year and 10-year “term premiums”. The narrow spread between the two - as we can observe below – suggests the compensation that investors get for the danger that inflation might accelerate over time is relatively lower for longer maturities, as we can see from the chart below. Not surprisingly, this seems to be consistent with a relatively fixed 2% target for inflation in the long term.

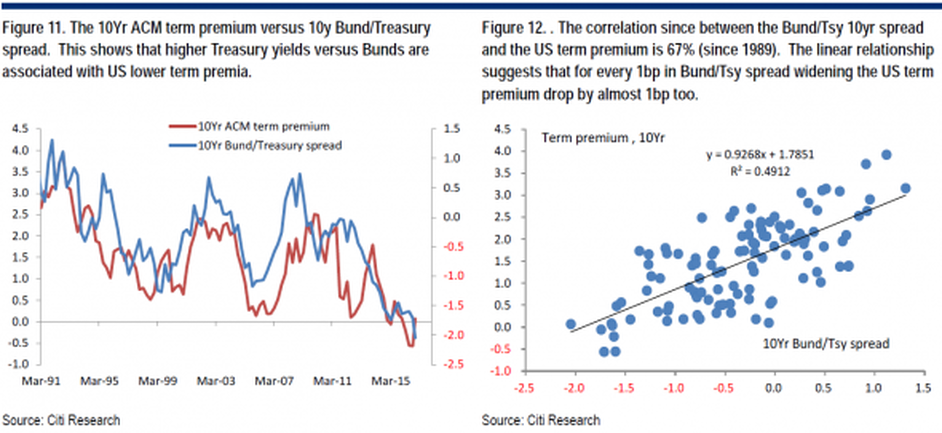

Furthermore, Citigroup has recently noticed an interesting relationship between the 10-year Treasury/Bund spread and the term premium implied by the NY Fed’s model.

What we can notice from the above chart is that when the spread between American yields and German ones widens, the implied “term premium” appears smaller, and vice versa. The main reason why this is likely to happen is that higher US yields attract foreign inflows that then compress the “term premium” along the yield curve.

From this point of view, investors should prefer longer maturities for US Treasuries. In fact, although the current divergences in the monetary policy between the Fed and the ECB are probably not going to last for a long time (as also the ECB has started a “tapering” by reducing the pace of its monthly repurchases), in the next months these are going to progressively increase foreign inflows that will compress the term premiums embedded in long-term US Treasuries.

Therefore, if interest rates increase – and this is what the market believes with a 98% probability – the back- end yields should increase relatively less than the front- end ones, at least in the short term. For this reason, long-only investors can preserve more value by reallocating part of their US Treasuries portfolios from a lower to a higher duration-based “bucket”.

Moreover, given that we previously noticed that the narrow difference between the implied 5-year and 10-year “term premiums” suggests investors get little compensation for the danger that inflation might accelerate significantly over time, it makes sense for investors to prefer 5-year rather than 10-year bonds on a relative basis.

Finally, as we discussed above, the term premium seems to be mostly linked to changes in the uncertainty about inflation forecasts. Since US inflation is expected to pick up quickly and significantly in the coming months, investors who are considering to take long positions in medium/long-term US bonds should seek some hedges against inflation. This point becomes even more important if we consider that generally back-end yields are more reactive to changes in inflation expectations, while front-end yields tend to be more dependent on the short-term effects of the Fed’s monetary policies.

As a consequence, medium/long-term TIPS can represent a reasonable investment for many institutional investors at the moment.

There are several strategies investors can follow in order to reallocate part of their portfolios to higher-duration securities.

Possibly, the most adequate in a rising interest rates environment are the barbell and the bond ladders.

The barbell is a buy-and-hold strategy in which money is invested in a combination of short-term and long-term bonds: as the short-term bonds mature, investors reinvest to take advantage of market opportunities while the long-term bonds provide attractive coupon rates.

Alternatively, what we can call the “bond ladders” is a strategy that is perhaps even more efficient in the current market environment. A laddered bond portfolio is invested equally in bonds maturing periodically, usually every year. As the bonds mature, money is reinvested to maintain the maturity ladder. However, what makes this strategy unique is that maturing short-term bonds are reinvested in bonds at the ladder’s long end, which typically offers higher yields. This can clearly be an advantage with rising interest rates.

To conclude, also long-only institutional investors can still play strategically in a rising interest rates environment and, eventually, even add value to their portfolios through spread trades along the yield curve together with appropriate hedges, especially against inflation risk.

Mattia Giammarusto