More than a decade has passed since the 2007, the year that deeply changed the economic and financial world and the way we look at it. No one will ever forget what happened after Lehman Brothers’ default and how rapidly the financial crisis infected all the branches of the economy, leading to the toughest recessions since the Great depression. It took policy makers several years to restore credibility and stability in the system and to push the economy into a new growth path.

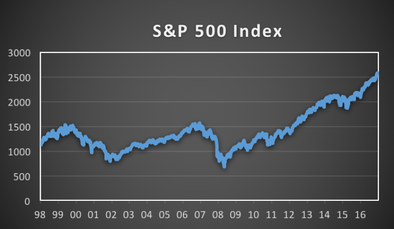

However, few people remember which signs made several economists foresee what was happening in the banking sector and which arguments they used to warn both political authorities and regulators. Today many of those signs have come over again and this time there are no excuses to ignore them. It is definitely necessary to analyse the hints taking the harmful effects into account and getting prepared to face any threats when the time comes. Firstly, the roaring stock market rally in the USA has reached a point where it is difficult to justify several market evaluations, while President Trump prefers to boast about it instead of considering the hidden menace. The following chart shows the S&P index over the last twenty years and compares the peaks reached before the 2000 and 2007 crisis with the current level, pointing out why policy makers should worry about a possible downturn.

However, few people remember which signs made several economists foresee what was happening in the banking sector and which arguments they used to warn both political authorities and regulators. Today many of those signs have come over again and this time there are no excuses to ignore them. It is definitely necessary to analyse the hints taking the harmful effects into account and getting prepared to face any threats when the time comes. Firstly, the roaring stock market rally in the USA has reached a point where it is difficult to justify several market evaluations, while President Trump prefers to boast about it instead of considering the hidden menace. The following chart shows the S&P index over the last twenty years and compares the peaks reached before the 2000 and 2007 crisis with the current level, pointing out why policy makers should worry about a possible downturn.

Moreover, again in the US, the repeal of the CFPB rule (Consumer Financial Protection Bureau) that would had strengthened the possibility of class actions against banks and other financial institution and the nomination of Jerome Powell as the new FED chairman might be the first step towards new deregulation policies, a potential hotbed for risky and dangerous investment strategies. Even if Europe is moving in the opposite direction through the enforcement of stricter rules about capital requirements and NPL management, it would be always exposed to overseas systemic financial instability.

Source: S&P, Data autonomously elaborated by the author

Source: S&P, Data autonomously elaborated by the author

Another key factor to be considered is that the easing monetary policies which prevented the global economy from collapsing might now be sowing the seeds of the next financial crisis. In fact, although economy has been performing quite well in recent times, interest rates are still close to zero both in the US and the Eurozone. While this enhances further growth, it might also generate serious threats for stability. Thanks to a favourable access to liquidity the worldwide amount of credit provided to the economy has surged and it is now reaching pre-crisis level. Although this benefits investments and GDP growth, it is also increasing banking sector exposure to an even slightly rise in companies’ default rate. In particular, emerging market’s debt outlook is getting worse, driven by China’s non-financial sector debt.

The chart shows the non-financial corporates debt to GDP ratio in EME’s countries, focusing on China’s worrying level. The situation looks even worse if you consider the growing credit provided to the corporate sector. IMF has recently found that the

“nominal credit to the nonfinancial sector more than doubled in the last five years, and the total domestic nonfinancial credit-to-GDP ratio increased by 60 percentage points to about 230pc in 2016, expected to reach 300pc by 2022” (1)

which is definitely not a sign of sustainable and long-lasting prosperity.

Non-financial corporates debt/GDP

Although Chinese central government has implemented several measures to bring the situation under control, the credit situation is still alarming due to a huge shadow banking activity. In a strongly interconnected global market, a financial shock coming from the emerging countries could easily spread all over the world, as it occurred in 2008. Despite many legislative dispositions have been set to strengthen banks’ resilience, the balance sheets of European banks are still burdened by large insolvent credits, and no one can assure whether they will be able to hold their own if a new shock strikes.

Meanwhile, the necessity of ending QE could be another serious threat. During the last press conference, the ECB President Mario Draghi has announced a downsizing of the asset purchase programme. Even if the ECB stated than interest rates will not be risen until the QE is over, the reaction of the market cannot be predicted, in particular towards those countries that have not solved their debt problems yet. If investors lose confidence, the hike in government bond interest rate will toughly hit their finances, so as to trigger a vicious cycle. In that case, we could assist to a new sovereign debts crisis, but this time ECB would have less tools to come to the rescue.

Indeed, the last point that weakens the current financial framework is the little scope monetary policy makers have to further help economy in case a new downturn occurs, given central banks’ enormous balance sheets and interest rates already very low. Wherever next crisis comes from- asset bubbles, credit glut, eastern countries or something else - it will be more difficult to rescue economy than it had been about a decade ago, and considering the consequences of that crisis, we cannot even imagine what would happen this time.

Lorenzo Monticone

(1) Tim Wallace; China’s debt boom could lead to financial crisis, IMF warns; http://www.telegraph.co.uk; 15 August 2017

“nominal credit to the nonfinancial sector more than doubled in the last five years, and the total domestic nonfinancial credit-to-GDP ratio increased by 60 percentage points to about 230pc in 2016, expected to reach 300pc by 2022” (1)

which is definitely not a sign of sustainable and long-lasting prosperity.

Non-financial corporates debt/GDP

Although Chinese central government has implemented several measures to bring the situation under control, the credit situation is still alarming due to a huge shadow banking activity. In a strongly interconnected global market, a financial shock coming from the emerging countries could easily spread all over the world, as it occurred in 2008. Despite many legislative dispositions have been set to strengthen banks’ resilience, the balance sheets of European banks are still burdened by large insolvent credits, and no one can assure whether they will be able to hold their own if a new shock strikes.

Meanwhile, the necessity of ending QE could be another serious threat. During the last press conference, the ECB President Mario Draghi has announced a downsizing of the asset purchase programme. Even if the ECB stated than interest rates will not be risen until the QE is over, the reaction of the market cannot be predicted, in particular towards those countries that have not solved their debt problems yet. If investors lose confidence, the hike in government bond interest rate will toughly hit their finances, so as to trigger a vicious cycle. In that case, we could assist to a new sovereign debts crisis, but this time ECB would have less tools to come to the rescue.

Indeed, the last point that weakens the current financial framework is the little scope monetary policy makers have to further help economy in case a new downturn occurs, given central banks’ enormous balance sheets and interest rates already very low. Wherever next crisis comes from- asset bubbles, credit glut, eastern countries or something else - it will be more difficult to rescue economy than it had been about a decade ago, and considering the consequences of that crisis, we cannot even imagine what would happen this time.

Lorenzo Monticone

(1) Tim Wallace; China’s debt boom could lead to financial crisis, IMF warns; http://www.telegraph.co.uk; 15 August 2017