Profit opportunities on Fed rates hike

From the time when the financial crisis broke out, the issue of Federal Reserve interest rates has not let investors sleep soundly. Since then, many variables came into play, making it incredibly difficult to forecast a possible outcome and leaving the other central banks resigned to a policy of very low rates.

However, new horizons are recently arising in the US economy (unemployment rate fell to 5% in November) spreading more and more the hope of a possible economic recovery.

Indeed, the strengthening of the US economy, together with the upbeat comments made by Janet Yellen are causing more people to be confident of a Fed rates hike in December. At the beginning of November, the Fed Chairwoman defined the decision of raising rates as a live possibility, since the US economy is expected to grow sufficiently to generate further improvements in the labour market and to return inflation rate to healthy levels.

What are the implications? From a simple macroeconomic view, as the national economy improves, bond yields go up and prices fall. Therefore, whenever the Fed is deliberately raising interest rates, a negative impact on bond prices will be taking place; high interest rates are the sign of a vigorous economy and they would mark the US as the first Western country to have recovered since 2008.

Hence, why has the Fed kept interest rates so low for almost a decade? The policy of lowering interest rates was an arranged reaction to the financial crisis broken out in 2008. Indeed, low interest rates mean basically more demand, as they spur the domestic aggregate demand (consumption + investments), stimulating people to spend and borrow more.

Since long-term bonds are more at risk now for losing value than shorter-term T-notes, investors may consider changing their investments from long-term bond funds to shorter-term funds, which, in the eventuality of a rates hike, will turn out to be cheaper and more profitable.

However, investing in T-bonds, because of the huge amount of capital it requires, is not affordable for everyone, but fortunately a valid alternative has been designed.

ProShares UltraShort 20+ Year Treasury ETF (TBT) is the name to describe an ETF designed to rise in value as US bond prices fall, offering opportunities to benefit from rising interest rates.

More specifically, TBT is calculated to obtain daily investment results that are two times the inverse (-2x) of the daily performance of the US 20+ Year T-Bond Index, which tracks investment results of an index composed of US T-bonds with remaining maturities greater than 20 years.

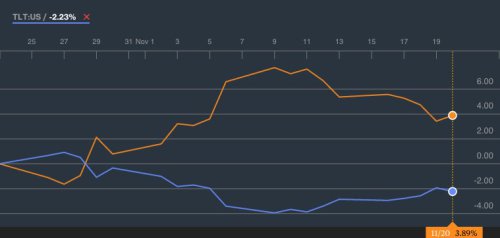

The symmetrical trend over the last month of the two ETFs is shown in the following graph (the orange line represents TBT).

From the time when the financial crisis broke out, the issue of Federal Reserve interest rates has not let investors sleep soundly. Since then, many variables came into play, making it incredibly difficult to forecast a possible outcome and leaving the other central banks resigned to a policy of very low rates.

However, new horizons are recently arising in the US economy (unemployment rate fell to 5% in November) spreading more and more the hope of a possible economic recovery.

Indeed, the strengthening of the US economy, together with the upbeat comments made by Janet Yellen are causing more people to be confident of a Fed rates hike in December. At the beginning of November, the Fed Chairwoman defined the decision of raising rates as a live possibility, since the US economy is expected to grow sufficiently to generate further improvements in the labour market and to return inflation rate to healthy levels.

What are the implications? From a simple macroeconomic view, as the national economy improves, bond yields go up and prices fall. Therefore, whenever the Fed is deliberately raising interest rates, a negative impact on bond prices will be taking place; high interest rates are the sign of a vigorous economy and they would mark the US as the first Western country to have recovered since 2008.

Hence, why has the Fed kept interest rates so low for almost a decade? The policy of lowering interest rates was an arranged reaction to the financial crisis broken out in 2008. Indeed, low interest rates mean basically more demand, as they spur the domestic aggregate demand (consumption + investments), stimulating people to spend and borrow more.

Since long-term bonds are more at risk now for losing value than shorter-term T-notes, investors may consider changing their investments from long-term bond funds to shorter-term funds, which, in the eventuality of a rates hike, will turn out to be cheaper and more profitable.

However, investing in T-bonds, because of the huge amount of capital it requires, is not affordable for everyone, but fortunately a valid alternative has been designed.

ProShares UltraShort 20+ Year Treasury ETF (TBT) is the name to describe an ETF designed to rise in value as US bond prices fall, offering opportunities to benefit from rising interest rates.

More specifically, TBT is calculated to obtain daily investment results that are two times the inverse (-2x) of the daily performance of the US 20+ Year T-Bond Index, which tracks investment results of an index composed of US T-bonds with remaining maturities greater than 20 years.

The symmetrical trend over the last month of the two ETFs is shown in the following graph (the orange line represents TBT).

In other words, for each loss in the T-bond prices, a double gain in TBT will be assured. Therefore, this potential ETF could become a great ally in the occasion of the decision to increase rates by the Fed. As mentioned above, this evaluation is getting more tangible.

With a brave play, the Fed could actually raise rates, returning to a policy of growth rather than of emergency. Moreover, the so-called ZIRP (Zero Interest Rate Policy) is an extremely harmful practice in the long run, as it is shown in Japan, where several recessions have taken place over the past 20 years.

On the other hand, the dramatic geopolitical situation in Europe and the consequent drop of the euro will definitely appreciate the dollar. This might urge US authorities to review even a possible devaluation of the USD, with a view of safeguarding national exports.

Filippo Maria Marino

With a brave play, the Fed could actually raise rates, returning to a policy of growth rather than of emergency. Moreover, the so-called ZIRP (Zero Interest Rate Policy) is an extremely harmful practice in the long run, as it is shown in Japan, where several recessions have taken place over the past 20 years.

On the other hand, the dramatic geopolitical situation in Europe and the consequent drop of the euro will definitely appreciate the dollar. This might urge US authorities to review even a possible devaluation of the USD, with a view of safeguarding national exports.

Filippo Maria Marino