Most of the world’s countries have recently been struggling with high inflation rates, due to the adverse macroeconomic events which have taken place in the last years. However, there is one country in particular which seems to struggle more than others: the United Kingdom. Why is such a powerful economy still trapped in the inflation spiral? What factors have led to this situation?

The UK’s History with Inflation

Recently Britain’s inflation became the highest in the G7 group, making it one of the most notable outliers among the advanced economies. Naturally, economists began to question the reasons behind this phenomenon to try and understand what possible factors could have such a drastic impact.

Historically, the UK has always managed to avoid any significant cases of hyperinflation. The highest inflation rates could be observed after the Napoleonic War, during the First World war (25%) and in the 1970s, when the inflation was affected by a drastic increase in oil prices and wage growth. Nevertheless, starting from the 1980s, the inflation stabilized and remained so for around two decades. The next unstable point was reached during the global financial crisis in 2008, when the inflation rose again because of the oil prices. However, in recent history, the most significant increase was recorded in 2022 with inflation rising to almost 10%. In this case, there is an entire list of factors that possibly lead to the current development of the situation. It is imperative to differentiate between the global and local factors.

In terms of local factors, experts believe that Brexit could be one of the reasons behind this trend. Particularly, due to Brexit, the UK has faced significant disruptions of imports in the food sector, as well as major worker shortage. These points will be discussed in more detail later in the article.

In terms of global factors, similar to the other European countries, the UK was heavily affected by the ongoing war between Russia and Ukraine. Besides all the political implications, in economic terms, the war caused a steady increase in energy prices. Moreover, Russia and Ukraine were active exporters of such essential goods as wheat, agricultural products, and metal. The war led to significant bottlenecks and further increased their prices in the market. It is important to mention that the war has worsened already existing supply chain disruptions, which were initially caused by the pandemic. All around the world, the factories were shut down, international trade was reduced, and most of the businesses significantly decreased their activity. In these conditions, most of the governments stepped in to support households to keep the economy alive, whilst the case of the UK, the government started to pay many workers’ wages through their famous “furlough scheme”. The latter allowed employers to benefit from heavy government support while employees did not notice any difference. As a result, many households accumulated increased savings, because of the lack of spending opportunities, which greatly increased their spending budget when the COVID-19 restrictions were lifted.

An interesting and unsuccessful approach to support the economy during the soaring inflation was proposed by one of the most recent British prime ministers Liz Truss. Instead of coming up with a proposition to reduce inflation, she introduced a plan to cut income taxes for the wealthiest segment of the population and significantly increase government spending. The biggest problem with this plan was that it was in direct interference with the monetary policy executed by the central bank, which was focused on bringing down the highest inflation seen in decades. As the package proposed by the prime minister was very unclear and could not support the economy without further increasing inflation, it only resulted in increased government debt and reduced revenue, and quickly led to her resignation.

Comparison With Other Economies

As the UK still experiences double-digit inflation its current situation looks notably worse than in other advanced economies. Even though inflation in the UK decreased from 10.4% in February to 10.1% in March , making a step in the right direction, recent developments in other economies look substantially more favorable. Average annual inflation in the Euro area decreased from 8.5% to 6.9% in the same period. Taking a closer look at the countries comparable to the UK, they seem to confirm the trend. For example, in March 2023 Germany's and France's inflation eased to 7.4% and 5.7% respectively. Even outside the Euro Area we see inflation slowing down, for instance the US has experienced a decrease from 6% in February to 5% in March.

As mentioned in the introductory paragraph, one reason why inflation is higher in the UK might still be associated with long lasting effects of Brexit. Some of the upward price pressure in February was due to food shortages, for example, of imported vegetables. As no shortage was recorded in the EU it seems likely that at least some of those problems can be connected to Brexit. Besides increased food prices, the trade barriers have led to more transaction time as well as bureaucracy for importing firms in general which is costly. Therefore, supply chain problems have generally worsened for the UK since Brexit and still have an impact on its current situation.

Another factor which increases costs today and might still be associated with Brexit is labor shortage. New research published in January 2023 in UK in a changing Europe suggests that even though migration of non-EU workers to the UK has picked up substantially after the COVID-19 pandemic, it cannot account for the loss of the additional EU workers during that time, had the UK stayed in the EU. The general trend in migration was disrupted by Brexit and it is estimated that the UK had 460,000 EU workers less in June 2022 than if it stayed in the EU. In comparison, the extra gain due to Brexit of non-EU workers only amounted to 130,000. Therefore, even though the workforce overall increased due to migration, this study suggests that it could have grown by an additional 330.000 workers if the UK did not leave the EU. Even though the study does not necessarily account for all variables, it gives a general idea how Brexit has worsened the current shortage especially of low

skilled workers. The tight labor market in turn leads to higher wages which need to be paid by firms to attract and retain employees.

Futhermore, the relatively weak British pound in comparison to the Euro is another factor which must be taken into consideration. As the UK generally had an overall trade deficit in recent years and its imports include many relevant goods, the low value of the pound has a big impact on the costs of consumers within the UK. In contrast, the strong US-Dollar reduced the costs for imports to the US and slowed inflation. The relatively low exchange rate in the UK also led to higher importing costs of energy commodities where prices were already high due to the conflict in Ukraine. In combination with the UK ́s reliance on natural gas imports for heating as well as electricity production, household bills increased substantially and made the UK particularly vulnerable to increases in gas prices. Even though gas prices have dropped again lately and quick relief for UK consumers seems possible the high costs still played a role in recent inflation.

Overall, it can be stated that most reasons for the inflation in the UK are similar to those in other advanced economies. However, Brexit, which led to a less resilient and more fragile economy, as well as and the low pound and UK ́s reliance on imported natural gas makes matters worse for the UK in comparison to other economies, which reacted better to the recent macroeconomic shocks.

Deep Dive in the Numbers

One can analyze the UK’s inflation from a more quantitative approach too, in order to obtain a broader view on the situation. A multitude of interrelated crises are playing out at the same time in the UK. Energy price spike and the aftermath of the Covid-19 pandemic have hit the country quite hard, resulting in the NHS now sustaining 7 million appointments and ordinary operations a year - up 75% from 2019. This has now become a macroeconomic problem, with surging prices the government has to face for the healthcare sector. Also, the current wave of strikes across the public sector and transportation have gained macroeconomic significance as the data show numbers of working days missed hit a peak since the ‘90s. These reasons have rendered Britain as a unicum between other advanced world economies, also thanks to its persistent inflation, that has been double digits for several months now.

Prime minister Rishi Sunak has promised to solve the problem by the end of the year and the BoE is set to increase interest rates again soon, but consumers are suffering. The lowest-income households have received several government packages and, according to NIESR, this resulted in a 2.3% net income gain. The middle class, on the other hand, is struggling without government help: monthly loan payments have skyrocketed, and the Office for Business Responsibility expects UK households' saving rates to almost drop to zero in 2023 and 2024.

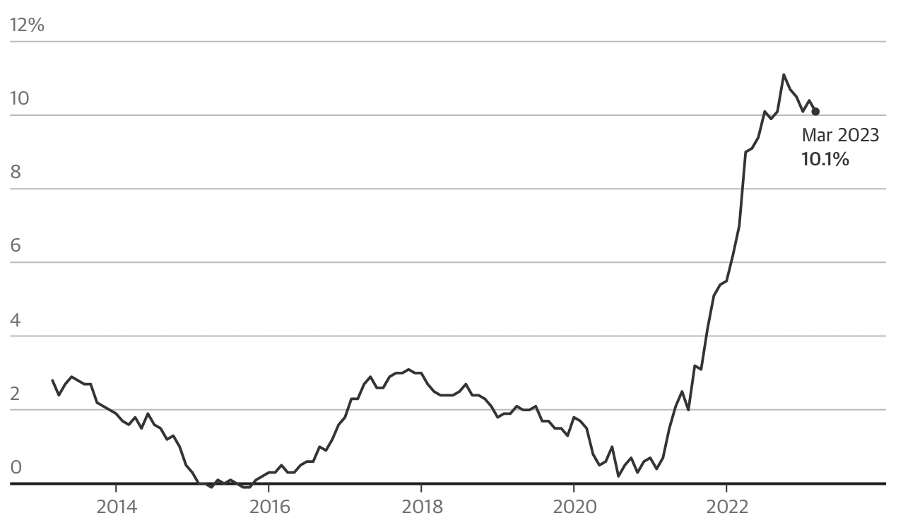

According to the Office for National Statistics (ONS) the CPI reached 10.1% in March, down from the 12.9% in February. Much higher than the 2% goal set by the BoE. A significant driver of inflation has been food prices, as indicated by the CPI for food and non-alcoholic beverages at 19.1% in March, up from 17.9% in February. The Core CPI, calculated excluding volatile sectors such as food and energy, rose to 8.2% in March, down from 9.2% in February. This implies that, although these two sectors are important drivers, underlying inflationary pressures are present and important too.

Recently Britain’s inflation became the highest in the G7 group, making it one of the most notable outliers among the advanced economies. Naturally, economists began to question the reasons behind this phenomenon to try and understand what possible factors could have such a drastic impact.

Historically, the UK has always managed to avoid any significant cases of hyperinflation. The highest inflation rates could be observed after the Napoleonic War, during the First World war (25%) and in the 1970s, when the inflation was affected by a drastic increase in oil prices and wage growth. Nevertheless, starting from the 1980s, the inflation stabilized and remained so for around two decades. The next unstable point was reached during the global financial crisis in 2008, when the inflation rose again because of the oil prices. However, in recent history, the most significant increase was recorded in 2022 with inflation rising to almost 10%. In this case, there is an entire list of factors that possibly lead to the current development of the situation. It is imperative to differentiate between the global and local factors.

In terms of local factors, experts believe that Brexit could be one of the reasons behind this trend. Particularly, due to Brexit, the UK has faced significant disruptions of imports in the food sector, as well as major worker shortage. These points will be discussed in more detail later in the article.

In terms of global factors, similar to the other European countries, the UK was heavily affected by the ongoing war between Russia and Ukraine. Besides all the political implications, in economic terms, the war caused a steady increase in energy prices. Moreover, Russia and Ukraine were active exporters of such essential goods as wheat, agricultural products, and metal. The war led to significant bottlenecks and further increased their prices in the market. It is important to mention that the war has worsened already existing supply chain disruptions, which were initially caused by the pandemic. All around the world, the factories were shut down, international trade was reduced, and most of the businesses significantly decreased their activity. In these conditions, most of the governments stepped in to support households to keep the economy alive, whilst the case of the UK, the government started to pay many workers’ wages through their famous “furlough scheme”. The latter allowed employers to benefit from heavy government support while employees did not notice any difference. As a result, many households accumulated increased savings, because of the lack of spending opportunities, which greatly increased their spending budget when the COVID-19 restrictions were lifted.

An interesting and unsuccessful approach to support the economy during the soaring inflation was proposed by one of the most recent British prime ministers Liz Truss. Instead of coming up with a proposition to reduce inflation, she introduced a plan to cut income taxes for the wealthiest segment of the population and significantly increase government spending. The biggest problem with this plan was that it was in direct interference with the monetary policy executed by the central bank, which was focused on bringing down the highest inflation seen in decades. As the package proposed by the prime minister was very unclear and could not support the economy without further increasing inflation, it only resulted in increased government debt and reduced revenue, and quickly led to her resignation.

Comparison With Other Economies

As the UK still experiences double-digit inflation its current situation looks notably worse than in other advanced economies. Even though inflation in the UK decreased from 10.4% in February to 10.1% in March , making a step in the right direction, recent developments in other economies look substantially more favorable. Average annual inflation in the Euro area decreased from 8.5% to 6.9% in the same period. Taking a closer look at the countries comparable to the UK, they seem to confirm the trend. For example, in March 2023 Germany's and France's inflation eased to 7.4% and 5.7% respectively. Even outside the Euro Area we see inflation slowing down, for instance the US has experienced a decrease from 6% in February to 5% in March.

As mentioned in the introductory paragraph, one reason why inflation is higher in the UK might still be associated with long lasting effects of Brexit. Some of the upward price pressure in February was due to food shortages, for example, of imported vegetables. As no shortage was recorded in the EU it seems likely that at least some of those problems can be connected to Brexit. Besides increased food prices, the trade barriers have led to more transaction time as well as bureaucracy for importing firms in general which is costly. Therefore, supply chain problems have generally worsened for the UK since Brexit and still have an impact on its current situation.

Another factor which increases costs today and might still be associated with Brexit is labor shortage. New research published in January 2023 in UK in a changing Europe suggests that even though migration of non-EU workers to the UK has picked up substantially after the COVID-19 pandemic, it cannot account for the loss of the additional EU workers during that time, had the UK stayed in the EU. The general trend in migration was disrupted by Brexit and it is estimated that the UK had 460,000 EU workers less in June 2022 than if it stayed in the EU. In comparison, the extra gain due to Brexit of non-EU workers only amounted to 130,000. Therefore, even though the workforce overall increased due to migration, this study suggests that it could have grown by an additional 330.000 workers if the UK did not leave the EU. Even though the study does not necessarily account for all variables, it gives a general idea how Brexit has worsened the current shortage especially of low

skilled workers. The tight labor market in turn leads to higher wages which need to be paid by firms to attract and retain employees.

Futhermore, the relatively weak British pound in comparison to the Euro is another factor which must be taken into consideration. As the UK generally had an overall trade deficit in recent years and its imports include many relevant goods, the low value of the pound has a big impact on the costs of consumers within the UK. In contrast, the strong US-Dollar reduced the costs for imports to the US and slowed inflation. The relatively low exchange rate in the UK also led to higher importing costs of energy commodities where prices were already high due to the conflict in Ukraine. In combination with the UK ́s reliance on natural gas imports for heating as well as electricity production, household bills increased substantially and made the UK particularly vulnerable to increases in gas prices. Even though gas prices have dropped again lately and quick relief for UK consumers seems possible the high costs still played a role in recent inflation.

Overall, it can be stated that most reasons for the inflation in the UK are similar to those in other advanced economies. However, Brexit, which led to a less resilient and more fragile economy, as well as and the low pound and UK ́s reliance on imported natural gas makes matters worse for the UK in comparison to other economies, which reacted better to the recent macroeconomic shocks.

Deep Dive in the Numbers

One can analyze the UK’s inflation from a more quantitative approach too, in order to obtain a broader view on the situation. A multitude of interrelated crises are playing out at the same time in the UK. Energy price spike and the aftermath of the Covid-19 pandemic have hit the country quite hard, resulting in the NHS now sustaining 7 million appointments and ordinary operations a year - up 75% from 2019. This has now become a macroeconomic problem, with surging prices the government has to face for the healthcare sector. Also, the current wave of strikes across the public sector and transportation have gained macroeconomic significance as the data show numbers of working days missed hit a peak since the ‘90s. These reasons have rendered Britain as a unicum between other advanced world economies, also thanks to its persistent inflation, that has been double digits for several months now.

Prime minister Rishi Sunak has promised to solve the problem by the end of the year and the BoE is set to increase interest rates again soon, but consumers are suffering. The lowest-income households have received several government packages and, according to NIESR, this resulted in a 2.3% net income gain. The middle class, on the other hand, is struggling without government help: monthly loan payments have skyrocketed, and the Office for Business Responsibility expects UK households' saving rates to almost drop to zero in 2023 and 2024.

According to the Office for National Statistics (ONS) the CPI reached 10.1% in March, down from the 12.9% in February. Much higher than the 2% goal set by the BoE. A significant driver of inflation has been food prices, as indicated by the CPI for food and non-alcoholic beverages at 19.1% in March, up from 17.9% in February. The Core CPI, calculated excluding volatile sectors such as food and energy, rose to 8.2% in March, down from 9.2% in February. This implies that, although these two sectors are important drivers, underlying inflationary pressures are present and important too.

UK CPI Index

Source: The Guardian

Source: The Guardian

Recently, even the Chief Economist of the BoE, Huw Pill, admitted that companies and households must accept that the current situation has made them poorer and added: “We’re all worse off”.

Forecast & Outlook

As can be understood from the paragraphs above, the current situation of inflation in the UK is worrying for many consumers and businesses, with rising prices impacting the cost of living for many people. This has led to many discussions about the impact of inflation on the UK economy and what measures might be taken to address it. Looking ahead, there are various forecasts being made about the future of inflation in the UK, with some economists predicting that inflation will continue to rise in the short term while others believe it will start to fall sharply. Alongside these predictions, there are also debates around the appropriate monetary policy response to inflation, with some arguing for tighter controls on interest rates and others advocating for more expansionary policies to support economic growth. As these discussions continue, it will be important for policymakers to carefully consider the various factors at play and make informed decisions about how best to manage inflation and support the UK economy in the months and years to come. In the next paragraph, we will examine the forecast for inflation in the UK and the implications for monetary policy.

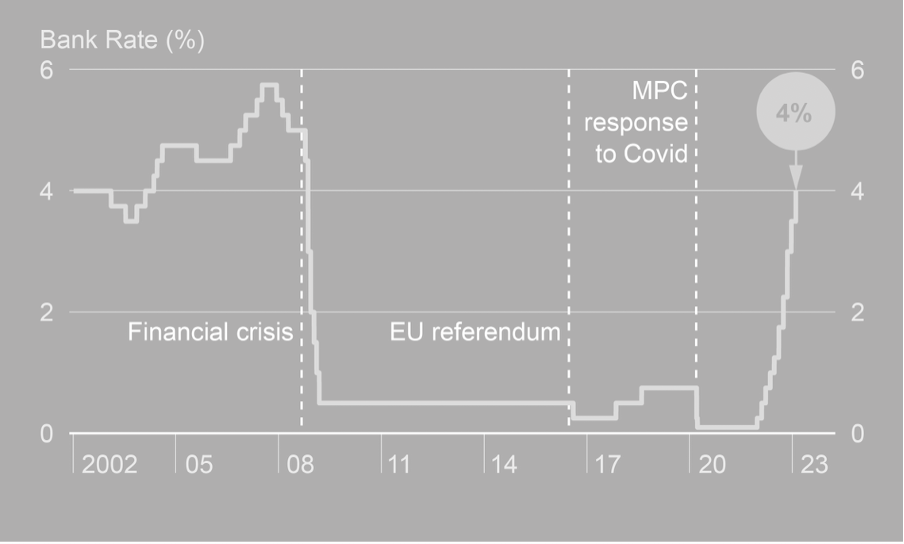

The Chancellor of the Exchequer (the minister of finance in the UK), Jeremy Hunt, mentions that the current levels of inflation are “dangerously high” and “we need to do everything we can to maintain our focus on bringing it down”. He is aiming to halve the inflation figure by the end of the current year. The Bank of England, which sets the monetary policy in the UK, seems to have the same vision, as they voted in their meeting ending on February 1st, 2023, to raise the Bank Rate again by 0.5 percentage points, to 4%, with a majority of 7-2 members voting in favor of the increase. The BoE’s overall goal is to decrease inflation to a stable 2% level. Although current inflation levels are very far from that, the BoE is confident that they can achieve this again in the medium term (i.e. approximately 3 years).

Forecast & Outlook

As can be understood from the paragraphs above, the current situation of inflation in the UK is worrying for many consumers and businesses, with rising prices impacting the cost of living for many people. This has led to many discussions about the impact of inflation on the UK economy and what measures might be taken to address it. Looking ahead, there are various forecasts being made about the future of inflation in the UK, with some economists predicting that inflation will continue to rise in the short term while others believe it will start to fall sharply. Alongside these predictions, there are also debates around the appropriate monetary policy response to inflation, with some arguing for tighter controls on interest rates and others advocating for more expansionary policies to support economic growth. As these discussions continue, it will be important for policymakers to carefully consider the various factors at play and make informed decisions about how best to manage inflation and support the UK economy in the months and years to come. In the next paragraph, we will examine the forecast for inflation in the UK and the implications for monetary policy.

The Chancellor of the Exchequer (the minister of finance in the UK), Jeremy Hunt, mentions that the current levels of inflation are “dangerously high” and “we need to do everything we can to maintain our focus on bringing it down”. He is aiming to halve the inflation figure by the end of the current year. The Bank of England, which sets the monetary policy in the UK, seems to have the same vision, as they voted in their meeting ending on February 1st, 2023, to raise the Bank Rate again by 0.5 percentage points, to 4%, with a majority of 7-2 members voting in favor of the increase. The BoE’s overall goal is to decrease inflation to a stable 2% level. Although current inflation levels are very far from that, the BoE is confident that they can achieve this again in the medium term (i.e. approximately 3 years).

UK Interest Rate Changes

Source: Bank of England

Source: Bank of England

They forecast that the annual CPI inflation will decrease to approximately 4% towards the end of the year. According to their latest model forecasts, if they were to increase rates further to 4,5% in mid-2023, decreasing them again over the course of the next three years, CPI inflation would decline again below the 2% level, mainly due to an increasing degree of economic slack and falling external pressures. However, there are considerable uncertainties surrounding this medium-term outlook, and the MPC still considers the risks to inflation to be skewed significantly to the upside.

Among conventional banks and asset managers, there are varying views on the size and shape of the decrease of inflation. While some institutions are optimistic about inflation falling back to normal levels soon, others remain cautious and expect a slower yet sustained decrease. Citi, for example, is one of the more aggressive forecasters, predicting that inflation could come down to 2% by the end of the year. However, analysts at wealth manager Charles Stanley have expressed suspicion that the UK's inflation is of the "stickier" variety, suggesting that reining in price rises without causing damage to the economy may be more challenging. The Organization for Economic Cooperation and Development (OECD) expects inflation to reach 4.5% by the end of the year.

In conclusion, there is a lack of consensus among banks, asset managers, and policymakers on the outlook for inflation in the UK. While some are hopeful that inflation will fall back to normal levels soon, others are more cautious and expect inflation to remain elevated for longer. The Bank of England's challenge will be to balance the need to control inflation with the need to support economic growth and employment, a task that will require careful consideration and analysis.

Conclusion

Overall, much like many other countries, the UK shows a high level of inflation due to macroeconomic factors such as the Covid-19 pandemic and the Russia-Ukraine conflict. These general elements are worsened by aforementioned events such as Brexit and its implications, whose consequences are reflected in quantitative data which highlights the impact the inflation has had on UK households and companies in general. The overall prediction is that inflation will come down over the course of the next few years, but there is no consensus among policy makers and banks on how fast this will happen.

By Leo Antlitz, Vittorio Granuzzo, Lilit Kalantar and Tobias Van Winkel.

Among conventional banks and asset managers, there are varying views on the size and shape of the decrease of inflation. While some institutions are optimistic about inflation falling back to normal levels soon, others remain cautious and expect a slower yet sustained decrease. Citi, for example, is one of the more aggressive forecasters, predicting that inflation could come down to 2% by the end of the year. However, analysts at wealth manager Charles Stanley have expressed suspicion that the UK's inflation is of the "stickier" variety, suggesting that reining in price rises without causing damage to the economy may be more challenging. The Organization for Economic Cooperation and Development (OECD) expects inflation to reach 4.5% by the end of the year.

In conclusion, there is a lack of consensus among banks, asset managers, and policymakers on the outlook for inflation in the UK. While some are hopeful that inflation will fall back to normal levels soon, others are more cautious and expect inflation to remain elevated for longer. The Bank of England's challenge will be to balance the need to control inflation with the need to support economic growth and employment, a task that will require careful consideration and analysis.

Conclusion

Overall, much like many other countries, the UK shows a high level of inflation due to macroeconomic factors such as the Covid-19 pandemic and the Russia-Ukraine conflict. These general elements are worsened by aforementioned events such as Brexit and its implications, whose consequences are reflected in quantitative data which highlights the impact the inflation has had on UK households and companies in general. The overall prediction is that inflation will come down over the course of the next few years, but there is no consensus among policy makers and banks on how fast this will happen.

By Leo Antlitz, Vittorio Granuzzo, Lilit Kalantar and Tobias Van Winkel.

SOURCES

- The Guardian

- ONS

- BBC

- TradingEconomics

- FT

- Bank of England

- Reuters